The Fed held rates steady again this week — and while some were hoping for a summer cut to inject life into a sluggish private market, most of us in the trenches weren’t holding our breath. If you’re building, developing, or deploying capital right now, you already know the drill: plan smarter, stay nimble, and figure out how to move projects forward in an environment where flexibility is everything.

No Cut, No Surprise — But Still a Drag

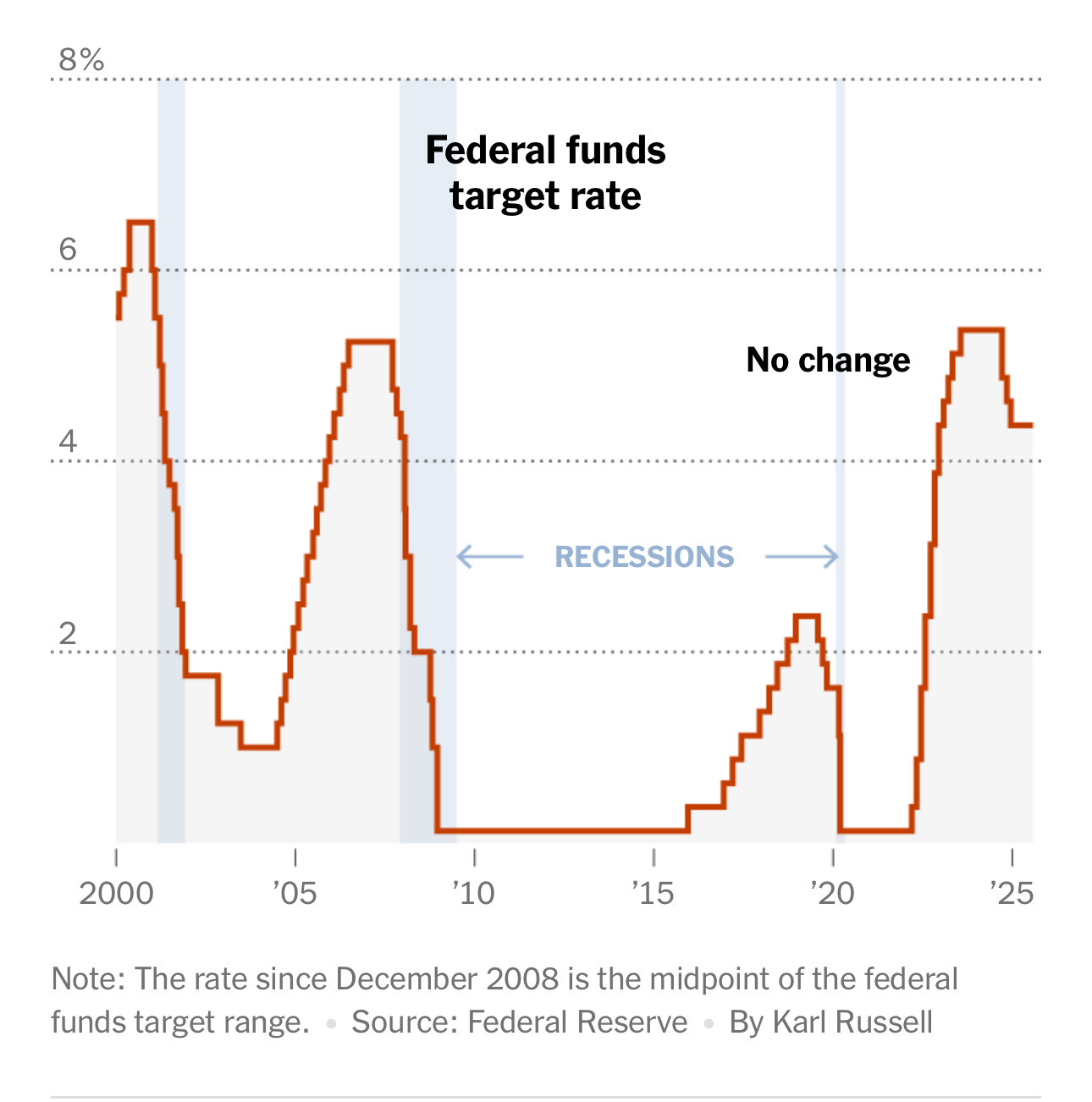

The Federal Reserve kept its benchmark rate unchanged at 4.25% to 4.5%, disappointing contractors and developers looking for a break. It’s the fifth straight meeting with no movement, and while that steadiness gives some predictability, it also reinforces the grind. For developers using floating-rate construction loans or trying to get deals to pencil under today’s capital stack realities, it’s a hard pill.

What’s more, political pressure on Fed Chair Jerome Powell is heating up — with President Trump calling out everything from rate policy to the $2.5 billion Fed HQ renovation. But drama aside, Powell isn’t budging, and we shouldn’t expect much in the way of rate relief until inflation data gives him more cover.

Private Projects Squeezed, Capital Getting Pickier

Traditional financing is still expensive, and capital partners are slower to move. As Joe Biasi at Newmark pointed out, projects that lean on floating-rate debt are especially exposed. Lenders are choosier, returns are tighter, and underwriting standards are stricter across the board.

We’re seeing the clearest pullback in the private sector, especially in commercial and market-rate multifamily. Value engineering is back in vogue. And in many cases, projects that would’ve launched a year or two ago are now sitting in a holding pattern.

But there’s nuance: some segments — like data centers, logistics, and manufacturing — are still surging, thanks in part to federal incentives and big-picture demand. That’s creating a bifurcated market where high-capex, mission-critical assets are powering ahead while traditional verticals lag behind.

Strategy Shift: Diversification, Flexibility, and Preconstruction Muscle

From my own seat as a developer and investor, the key right now is controlling what you can. That starts with early feasibility analysis, tight preconstruction planning, and flexible execution models. Self-performing certain trades, design-build contracts, and collaborative GMP approaches are all tools that can unlock speed and reduce surprises.

Others in the field are echoing that sentiment. Robert Brown at GCM Contracting Solutions says they’re leaning heavily on design-build delivery and internal concrete teams to maintain schedule control. At Adolfson & Peterson, early buyouts, proactive value management, and developer collaboration are keeping deals alive despite rising costs and financing headwinds.

It’s not just about shaving cost — it’s about preserving optionality. Phased construction, delayed verticals, and leaner spec packages are all part of the playbook now.

Developers Are Talking Timing, Capital Stack, and Exit Reality

At the developer level, the conversation has shifted from “Can I build this?” to “Can I exit this?” Everyone is recalibrating timelines and exit cap assumptions. We’re underwriting deals more cautiously and running sensitivity analyses on everything from construction duration to lease-up velocity.

Patrick Chesser at Ryan Companies summed it up well: “We’re pricing in today’s rate environment and avoiding political bets. If the fundamentals work, we move. If not, we wait.”

That’s a message more investors need to hear. Too many are still looking for 2021 returns in a 2025 cost environment. Smart capital is getting selective but staying active — especially where there’s pre-leasing, credit tenants, or public/private partnerships that bring additional layers of certainty.

Public Work as a Buffer

With private capital tightening, we’re seeing a heavier pivot toward public work — especially infrastructure, education, and civic projects funded through federal dollars or municipal bonds. These jobs may not be sexy, but they offer reliable timelines, lower risk, and crucial backlog.

Peter Dyga of ABC Florida notes the shift clearly: contractors are prioritizing public sector work because it offers more predictable cash flow and less financing volatility. That’s not to say private development is dead — just that the mix is changing.

The Inflation Wildcard

While rates stayed flat, the real concern remains inflation. Material costs are still volatile. Copper wire is up over 10% year-over-year, and a basket of 21 core inputs is tracking at a 2.5% increase mid-year — nearly the same pace we saw in 2023 and 2024.

If inflation reaccelerates, it won’t just delay cuts — it could trigger further tightening or spread risk pricing in the debt markets. That’s why everyone’s watching commodity trends and labor constraints just as closely as the Fed’s next move.

Looking Ahead: Don’t Wait on the Fed

Yes, a cut could come in Q4. But no one should be building their strategy around it. The winners in this environment — whether you’re a contractor, developer, or investor — are those who are underwriting conservatively, executing tightly, and finding ways to create certainty in an uncertain world.

We’re not in a market that rewards speed — we’re in a market that rewards preparation, adaptability, and strategic patience.

The Fed’s holding steady. So are we.