In the first half of 2025, nearly all U.S. GDP growth came from one place—data centers. According to Harvard economist Jason Furman, investment in AI and data infrastructure accounted for a staggering 92% of GDP growth, even though the sector represents only about 4% of total output.

Strip away that contribution, and the American economy would have been nearly flat—growing at just 0.1% on an annualized basis. That single statistic says more about where we’re heading than any Fed speech or jobs report.

We’re watching the U.S. economy become increasingly powered by servers, semiconductors, and AI clusters—not factories, retail stores, or even traditional construction.

The AI Economy’s Overweight Effect

What’s driving this? The hyperscalers.

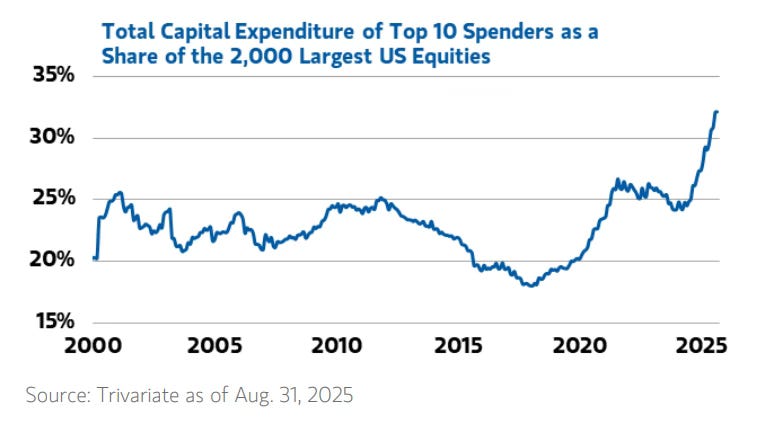

Amazon, Microsoft, Google, Meta, and Nvidia are spending at levels that rival national infrastructure programs—collectively approaching $400 billion annually in data center capital expenditures.

That spending alone is now adding roughly one full percentage point to U.S. GDP growth, according to Morgan Stanley CIO Lisa Shallet. In other words, without hyperscaler expansion, we’d be in a mild recession.

As a developer, I see this every day: land, power, and cooling have become the new gold. Entire cities are competing to attract data centers, offering incentives and grid access like they once did for manufacturing plants. What used to be a niche asset class is now at the core of the economic engine.

A Narrow Growth Story

This kind of concentrated growth is both powerful and risky.

Outside the tech infrastructure buildout, most other sectors are either stagnant or declining. Manufacturing has cooled. Retail is soft. Real estate construction—especially in housing—remains burdened by financing costs and supply constraints.

Even with falling interest rates, there’s little evidence of broad-based recovery. The AI sector is masking a weak underlying economy, and that imbalance can’t last forever.

Is It a Bubble—or a New Foundation?

It’s tempting to call this a bubble. Even Jeff Bezos has used that term when talking about the scale of AI infrastructure spending. But unlike past tech bubbles built on speculation, this one is grounded in tangible assets: energy, land, hardware, and physical capacity.

Data centers aren’t memes or app startups—they’re the backbone of the digital economy. The real question is whether the current level of spending is sustainable before returns normalize.

For investors and developers, this moment mirrors the early interstate highway era: massive, transformative investment with uncertain long-term winners. Those who build the right infrastructure in the right locations—where power, policy, and proximity align—will define the next decade of economic growth.

Why It Matters

At Kaufman Development, we look at this trend not as a tech story but as a real estate and energy story. The AI buildout is reshaping land use, power grids, and regional growth patterns in real time.

It’s also revealing a new economic truth: AI infrastructure has become America’s growth engine. Every megawatt deployed, every substation upgraded, every data hall built—it all contributes directly to GDP.

The challenge ahead is ensuring that this growth translates into broader economic strength, not just higher market caps for five companies.

Because right now, without data centers, the U.S. economy wouldn’t just be growing slower—it might not be growing at all.