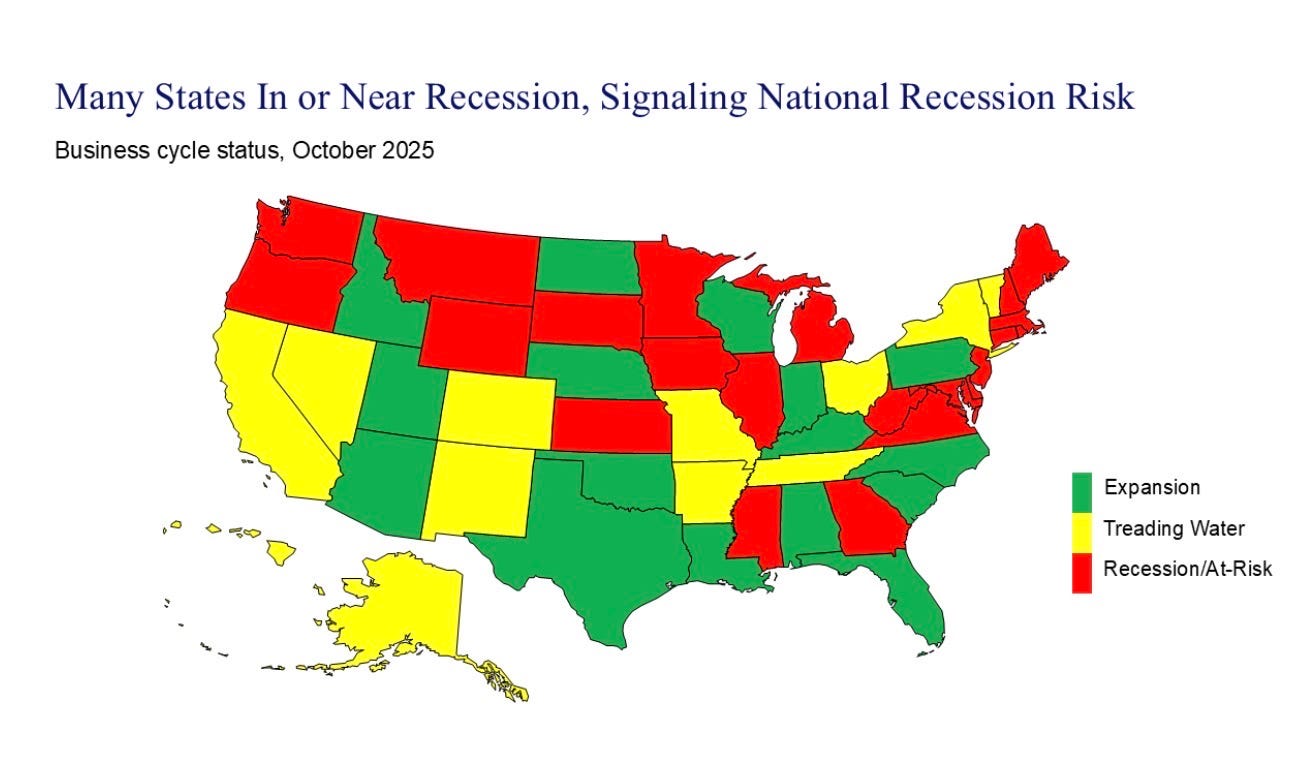

We often talk about national trends in economic growth and decline as though the U.S. were one monolithic entity. But once you peel back the layers, you realize the story is far more regional—and, in many cases, far more concerning. According to Mark Zandi, Chief Economist at Moody’s Analytics, 22 states—and the District of Columbia—are already in contraction or teetering on the edge, with an additional cohort essentially “treading water.”

That may not immediately scream “real estate developer alarm,” but when you consider that these states represent roughly one-third of the national GDP, the implications for development, capital, construction pipelines and market risk become unmistakable.

The Drivers Behind the State-by-State Divergence

What’s pushing this uneven performance? Here are the main vectors:

-

States heavily reliant on goods-producing sectors, agriculture, light manufacturing, and exposed to trade/tariff risks. These sectors are under pressure, and those states are showing up in Zandi’s “recession” bucket.

-

States with strong population inflows and service-economy momentum—think Texas, Florida—are faring comparatively better.

-

Big‐economy states like California and New York are currently treading water. They’re neither booming nor collapsing—but given their weight in the national economy, if they slip, it could tip the scale.

Why This Matters for Real Estate & Development

-

Capital access and investor confidence shift faster than project timelines. If a state’s economy is sagging (or perceived to be), risk premiums rise, lenders tighten, and certain projects get repriced or shelved.

-

Construction and entitlement pipelines in stressed states will feel this first. Permitting slows, cost inflation bites harder, and exit strategies become more fragile.

-

Market segmentation gets clearer. As some metros cool, others heat up. If you’re operating coast-to-coast (as you are with our platform spanning LA, Dallas, Detroit, Raleigh, Jacksonville, etc.), you must sharpen your filters—not all markets are created equal in this environment.

-

Timing becomes critical. With many states already in contraction, the priority becomes not just “what to build,” but where and when. Markets that are “treading water” but large in GDP share present large systemic risk if they slide.

Strategic Takeaway

For operators, investors, and developers the takeaway is simple:

-

Lean into the outperformers. Markets with structural tailwinds—population growth, service economy, modular friendly environments—are likely to absorb capital and complete product more cleanly.

-

Heighten your underwriting discipline. In states flagged by Zandi’s index, build extra buffers into cost escalation, leasing ramp, and exit timing.

-

Geo-diversify intelligently. Having a national footprint gives you optionality—but you still need to read the map. One or two large states faltering could ripple into national risk.

-

Visualize the full lifecycle impact. An economic slowdown doesn’t just hit occupancy—it affects sourcing, construction timelines, supply chain, financing, and exit multiples.

Final Word

We’re not announcing a national recession just yet—and Zandi doesn’t either. But to quote his words: “We’re on the precipice.”

As someone who builds, invests, and structures capital across the full development lifecycle, this should raise a clear signal: not all geographies are equal today, and the difference between advancing a project and deferring one may hinge on location and timing more than ever.

Stay sharp. Stay selective. And let the data guide your next move.