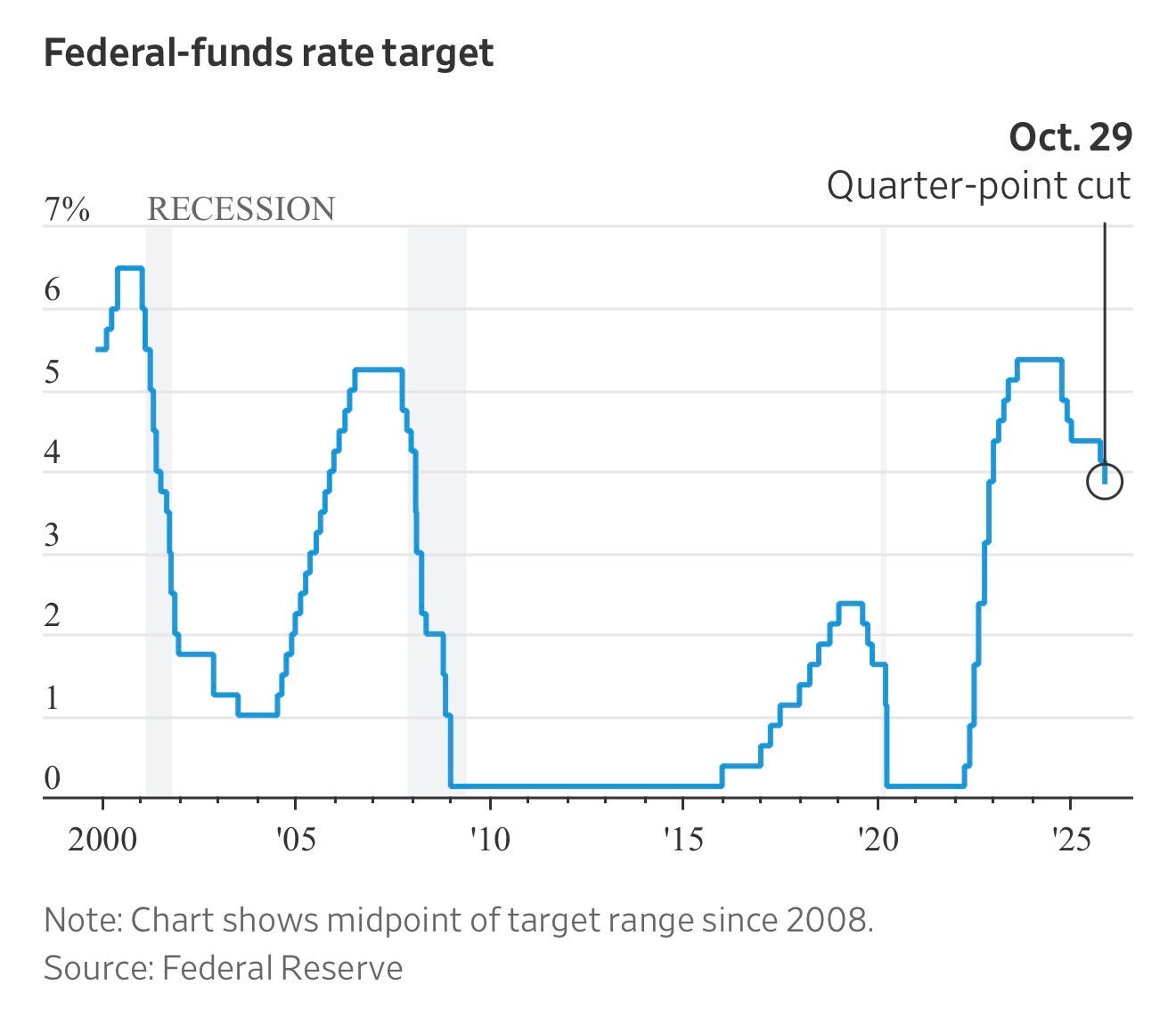

The Federal Reserve just cut interest rates for the second time this year, lowering its benchmark rate to a range between 3.75% and 4% — the lowest in three years. The move signals growing concern that the labor market is cooling faster than expected, even as inflation remains stubborn in pockets of the economy.

But this cut isn’t about creating another wave of cheap capital. It’s about damage control. The Fed is navigating blind, with much of the government still shut down and official labor and inflation data unavailable. Powell described the situation as “challenging” with “no risk-free path,” and that’s exactly how it feels for those of us trying to underwrite deals in real time.

A Softer Labor Market — and a Structural Shift

Job growth has slowed sharply. Powell suggested part of that is due to a smaller labor force — a result of reduced immigration since 2020. Fewer workers entering the U.S. means employers don’t have to add as many jobs to keep unemployment steady.

This matters because it changes the way the Fed — and the rest of us — interpret job data. In a normal cycle, monthly job growth below 100,000 would trigger alarm bells. But with immigration still lagging, the economy might only need 50,000 new jobs per month to stay in balance.

Former St. Louis Fed President James Bullard put it plainly: “I don’t know that everyone has really adjusted to that.” Neither have markets — or developers still trying to assess real demand for housing, retail, and industrial space in regions reshaped by labor shortages.

Rates, Tariffs, and the Cost of Building

For developers, rate cuts are always a double-edged sword. Lower borrowing costs help on paper, but the reasons behind the cuts — slower growth, weaker job creation, policy uncertainty — often offset those benefits.

At the same time, tariffs are re-entering the conversation. Powell acknowledged that while tariffs are typically seen as one-time price shocks, their inflationary effects “could be more persistent.” For construction and manufacturing, that means costs could stay elevated even as rates fall.

Steel, aluminum, glass, and electrical components — all critical to multifamily and mixed-use development — remain subject to tariff exposure. Combine that with the 12% annual increase in insurance premiums across the multifamily sector, and you have the recipe for a fragile build environment: cheaper debt, but more expensive everything else.

Developers Are Navigating a Split Reality

On one side, rate cuts may reopen lending pipelines and improve deal feasibility, particularly for refinancings and stabilized assets. On the other, underwriting new projects is getting harder, with higher replacement costs and slower rent growth.

That tension is showing up in bids and construction timelines. Many developers are sitting on land they could build today — but won’t, because cost certainty is gone. Materials, labor, and insurance remain volatile, and tariffs inject yet another layer of unpredictability.

The irony is that while the Fed is trying to prevent a recession, its actions could further distort the real estate cycle — encouraging short-term refinancing activity while slowing new construction starts, especially in high-cost coastal markets.

What to Watch Heading Into 2026

If the Fed keeps cutting through year-end, we’ll likely see a temporary reprieve in lending spreads. But the fundamentals of the development equation — materials, insurance, and regulatory risk — are moving in the opposite direction.

For real estate developers and investors, the opportunity in this environment isn’t in chasing yield; it’s in underwriting discipline and strategic timing. The next 12–18 months will favor players who can:

-

Lock in financing early while spreads narrow.

-

Source domestically to reduce tariff exposure.

-

Leverage modular and offsite construction to offset labor shortages.

-

Target markets with sustained employment drivers, not just rate-driven momentum.

The Fed can lower rates, but it can’t rebuild the supply chain or stabilize insurance markets. For those of us on the ground, that means the cost of capital may ease — but the cost of building likely won’t.

And that’s where the next real opportunity lies.