Why the Coming 50% Surge in Global Capacity Will Reshape Real Estate, Power Markets, and Institutional Investment

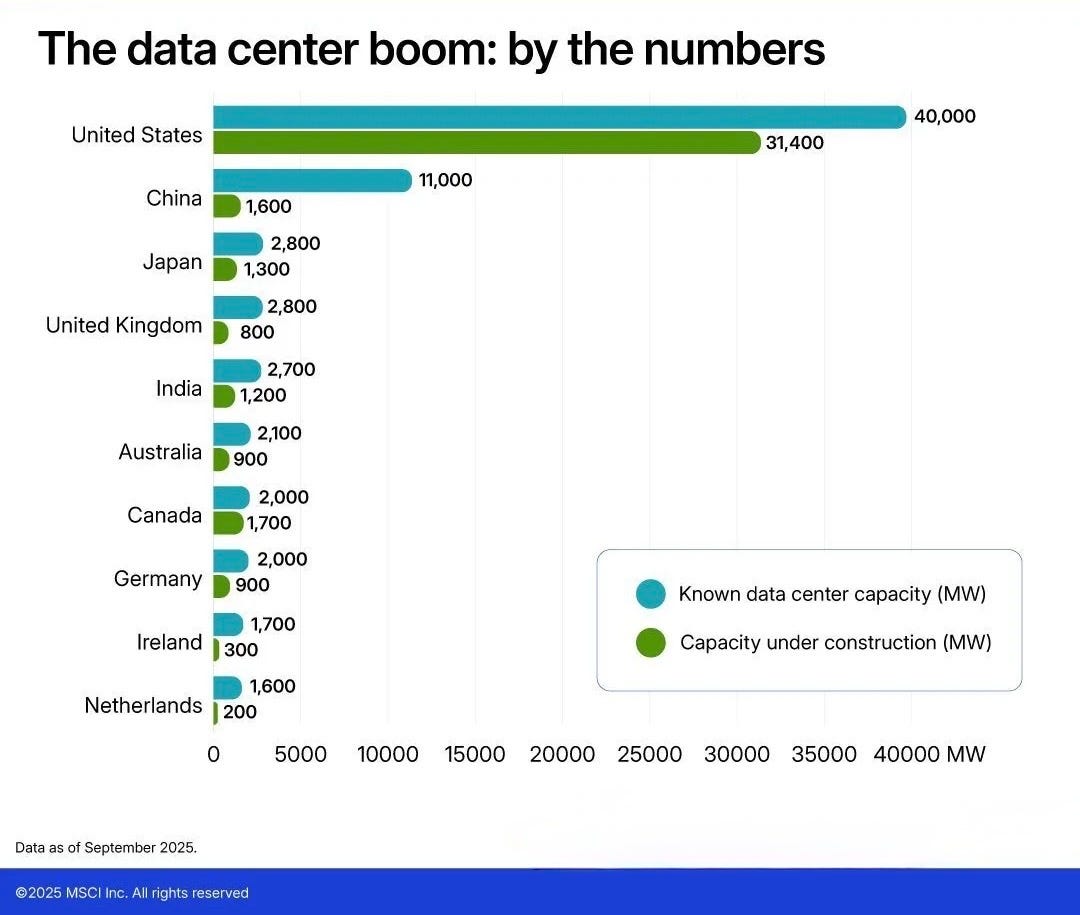

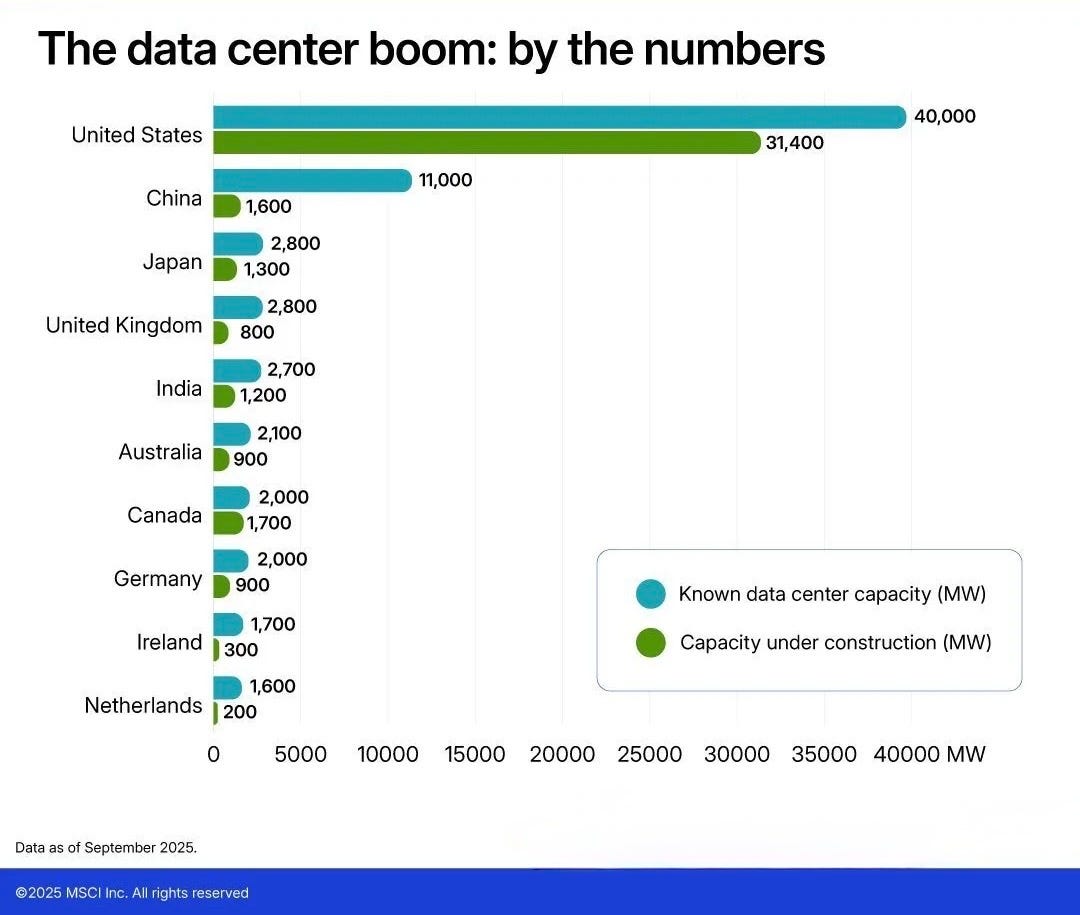

Global data center development is entering its most aggressive expansion cycle in history. More than 47,000 megawatts of capacity is now under construction worldwide—representing roughly $550 billion of end value and a 50% increase in total global supply once completed. The U.S. is leading the charge, but every major market with the power, land, and fiber infrastructure to support hyperscale growth is building at unprecedented speed.

The investment thesis is clear: AI, machine learning, cloud computing, autonomous systems, and global digital infrastructure demand more compute than the existing fleet can ever provide. Capital is flowing into development rather than acquisition because the market has realized there simply isn’t enough institutional-quality, large-scale data center inventory to buy.

But behind the bullish consensus lies a more complicated truth. The rapid expansion of data centers raises profound questions about the capacity of global power grids, the future of carbon intensity in real estate portfolios, and whether the pace of development can continue without major structural changes to how digital infrastructure is powered.

This is not just an opportunity story. It is also a warning.

The Scale of Growth Is Unlike Anything in Modern Real Estate

Investors have deployed more capital into data center development in the past three years than in the previous decade combined. The numbers tell the story:

47+ gigawatts under construction globally

$550 billion in total value—five times the cumulative volume of acquisitions since 2007

12+ GW added in the first half of 2025 alone

Global capacity set to grow by ~50% when current projects go live

This is the largest single asset-class expansion in modern real estate history. And unlike office, multifamily, or retail, the drivers of demand are not human behavior—they’re technological inevitabilities.

AI models are doubling in complexity every 3–6 months. Cloud workloads continue to compound. Every enterprise is digitizing. Governments are building sovereign AI systems. Companies like Meta, Alphabet, Microsoft, Amazon, and Apple are deploying capital at a scale no traditional real estate operator can match.

The long-term demand story is unquestioned.

But demand alone doesn’t solve the biggest challenge facing the sector: energy.

The Grid Problem: Can Power Systems Keep Up?

Data centers already consume 1.5% of global electricity—more than the entire annual energy use of France. The International Energy Agency estimates that number will double by 2030, reaching roughly 3% of global capacity.

Out of that increase, 40% is expected to come from coal and gas, given current grid mixes and build-out timelines.

This is where the opportunity runs headlong into structural risk.

High-growth markets are facing grid stress today

Ireland: Data centers consumed 22% of national electricity in 2024, up from 5% in 2015.

United States: New facilities under construction could add 2.6% to national emissions.

Southeast Asia: Markets like Malaysia and the Philippines are experiencing unprecedented power constraints as hyperscalers and private equity chase regional capacity.

This grid strain is no longer an abstract future risk—it is already influencing permitting timelines, utility procurement strategies, and geographic siting decisions.

The question for investors is no longer “Will demand grow?” It’s “Can the grid support it?”

The Sustainability Dilemma for Institutional Capital

Data centers were ranked the #1 target for global property investors in 2025 (ULI/PwC), yet they also represent one of the highest-carbon-intensity asset classes in real estate.

Here’s the tension:

Leading institutional buyers—Brookfield, AXA, Goldman Sachs, CBRE IM, CPP Investments, Invesco—have committed to science-based or net-zero targets.

But a 50-MW hyperscale data center carries the carbon footprint of roughly 100 energy-efficient office buildings.

Grid electricity mixes vary widely, meaning location-based emissions often dwarf the impact of renewable energy certificates or PPAs.

Put simply: a shift toward data centers makes meeting portfolio decarbonization targets significantly harder.

Many operators report low “market-based” emissions through PPAs or RECs, but the physical grids powering these facilities remain carbon-intensive, especially in regions like Northern Virginia, Texas, and parts of Europe and Asia.

Investors now face a fundamental question:

Can an asset class central to the future of global technology align with net-zero commitments that were designed for yesterday’s real estate?

Development Is Outpacing Renewable Energy

A structural challenge is hiding in plain sight:

Data center development is growing faster than global renewable energy deployment.

Even with record renewable additions, fossil fuels are expected to account for over 40% of the additional electricity needed for AI-driven data center growth.

That gap has several consequences:

Portfolio carbon intensity rises, even with efficiency gains.

Regulators may shift to location-based reporting, reducing the usefulness of RECs.

Operators need firm, 24/7 power, not intermittent renewables.

Low-carbon PPAs become fiercely competitive, driving up price.

New nuclear, hydro, and geothermal infrastructure becomes essential.

In other words, this is no longer just a real estate challenge—it is an energy infrastructure challenge.

The Opportunity: This Is a Generational Build-Out

Despite the risks, the upside is enormous. The world needs:

More compute

More storage

More edge sites

More power

More cooling innovation

More fiber and interconnection

More sovereign infrastructure

And unlike many real estate sectors, this demand is not cyclical. It does not rely on consumer sentiment or job growth. It is structural and accelerating.

Where the most powerful opportunities lie

1. Development over acquisition

There is simply not enough existing supply, which is why new construction continues to dominate capital flows.

2. Power-secure regions

Markets with reliable low-carbon baseload power—e.g., hydro, nuclear, geothermal—will become the most defensible.

3. AI infrastructure partnerships

Hyperscalers increasingly want integrated partners who can deliver land, power, construction, and operations at scale.

4. Battery storage and microgrid innovation

These will become essential to stabilizing loads and managing 24/7 availability.

5. Real estate platforms that bridge energy and computing

The future winners will not be traditional developers—they will be companies treating data centers as part of a broader energy + digital ecosystem.

This is the direction my own platform is moving: aligning real estate, infrastructure, AI demand, and energy strategy into a single development thesis.

The Concern: The Industry Must Acknowledge Its Blind Spots

For all the enthusiasm, several pressure points demand sober analysis:

Grid strain is real and could bottleneck development in top markets.

Carbon intensity could threaten institutional capital flows as reporting standards tighten.

Permitting timelines are lengthening as utilities struggle to meet load requirements.

Renewable supply is not keeping pace with hyperscale growth needs.

Siting decisions are now as much about power procurement strategy as they are about land and fiber.

The industry cannot simply build its way out of these issues.

The next decade will be defined by who can secure long-term, clean, reliable power—not just who can pour concrete.

The Bottom Line

The global data center boom represents one of the largest real estate and infrastructure opportunities of the century. But it also introduces a set of risks that are broader than anything the sector has confronted before.

The opportunity is clear: rising demand, structural growth, long-duration cash flows, and a once-in-a-generation development cycle.

The concern is equally clear: grid strain, rising emissions, regulatory pressure, and the growing tension between the digital economy and global climate commitments.

Navigating both requires more than capital. It requires an energy strategy.

And in the era of AI, energy is the new location.