The construction industry is heading into 2026 with more volatility, more constraints, and more structural pressure than most analysts care to admit. JLL’s latest outlook, combined with fresh data from ConstructConnect and Dodge, paints a picture that every developer, contractor, lender, and investor should be paying attention to.

For those of us actively building across the country, none of this is theoretical. These pressures are showing up in live budgets, subcontractor availability, bid spreads, and capital-stack decisions. And the gap between macro commentary and what’s actually happening on job sites continues to widen.

In 2026, navigating this market will require a different level of discipline and agility than even the last three years demanded.

Trade and Immigration Policy Are Rewriting Project Feasibility

JLL is blunt on this point: construction will not find solid footing in 2026.

The headwinds aren’t short-term or cyclical, they are structural.

Trade policy, tariff volatility, and immigration restrictions have converged to reshape the cost of materials, the availability of labor, and the reliability of schedules. These are no longer isolated shocks, they are system changes.

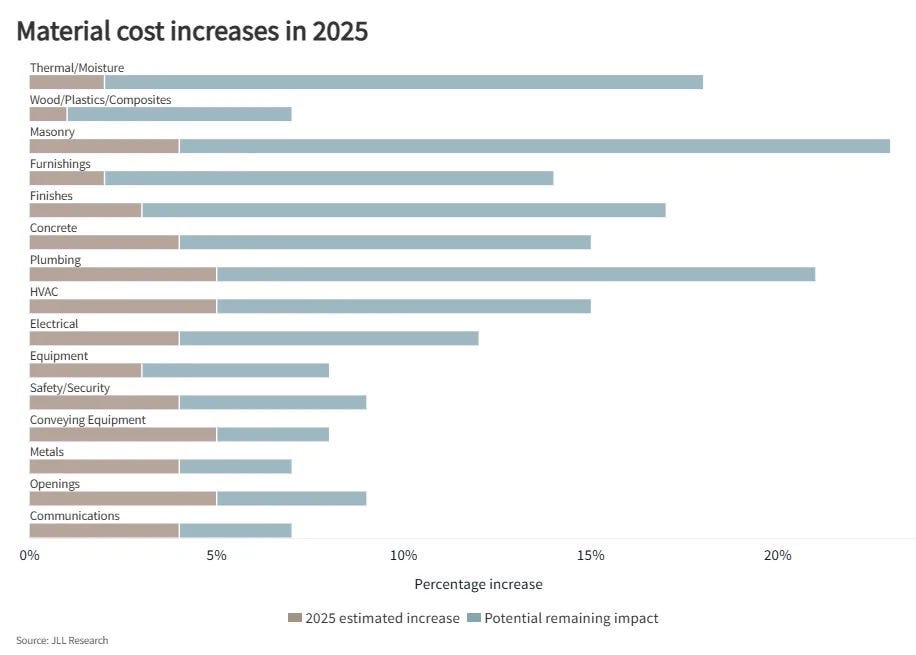

Materials remain unpredictable. Even though cost growth slowed below 1 percent in 2025, that slowdown is misleading. Construction costs are still up 39 percent since 2020, far outpacing general inflation. Tariffs and sourcing constraints ensure materials remain a wild card well into 2026 and probably 2027.

Labor constraints are even more disruptive. We are working with an aging workforce, too few new entrants, and tighter immigration policy. JLL forecasts that by 2026, non-residential construction job growth effectively flatlines at 0.03 percent. And anyone running bids right now knows this already: labor availability is becoming the single biggest local differentiator.

Some markets will have enough labor to function. Others won’t. Development timelines and pro formas will increasingly reflect that reality.

Project Abandonments Are Rising Fast — A Clear Warning Signal

ConstructConnect’s November data confirms what many of us have been sensing: the strain is showing.

Project abandonments surged 41.1 percent month-over-month, pushing the Project Stress Indicator to its highest level since July. The year-over-year abandonment rate is now up nearly 10 percent. The reason is straightforward — many developers stocked up on materials earlier in the year to stay ahead of tariffs, and those reserves are now depleted.

Once the stockpiles dried up, the true cost of new procurement hit pro formas hard enough to make some projects unworkable.

Private sector projects are taking the biggest hit, up 5.7 percent year-over-year in abandonments. The public sector dipped slightly, but that strength won’t offset the private-market pullback. Delays also jumped 16.5 percent from October, indicating widespread hesitation.

For sponsors, lenders, and GC partners, this data is a flashing red light: feasibility models are breaking more quickly, and more often.

Megaprojects Are Keeping the Headline Numbers Alive

Despite the turbulence, the construction industry is not collapsing. Dodge reports a 21 percent jump in construction starts in October, but the drivers matter: billion-dollar data center and manufacturing megaprojects.

These projects are distorting the national picture:

Meta’s $7.5 billion Hyperion data center in Louisiana

Eli Lilly’s $1.7 billion manufacturing plant in Indiana

These builds are essential, and they are propping up national construction activity. But they also create a two-tier market: well-capitalized institutional megaprojects are accelerating, while many mid-size and private projects stall out.

This divergence is going to be one of the defining themes of 2026.

Residential: A Sector Under Intensifying Stress

Residential construction is weakening again.

Activity is down 15 percent overall.

Multifamily, once the growth engine of U.S. development, saw a 39 percent plunge in starts. Single-family managed a modest 2 percent gain, which reflects both changing household preferences and the financing environment.

Developers are still bullish on housing long term and JLL expects residential spending to grow from $860 billion to $940 billion by 2027, but near-term momentum is clearly slowing. Multifamily remains challenged by elevated supply in key Sun Belt metros, higher operating costs, and tighter underwriting from lenders.

Those who build, acquire, or restructure residential assets need to recognize that 2026 will not be a smooth year.

The Complexity Premium: Why Execution Matters More Than Ever

The common theme across all these datapoints is complexity.

Not crisis, not collapse — but complexity.

We are entering a period where:

Cost certainty is increasingly rare

Labor availability varies widely by region

Tariff-driven supply risk is back

Large projects skew national data

Mid-size developments face capital constraints

Schedules now hinge on local policy, labor pools, and supply channels

Strong developers will not attempt to force projects into outdated assumptions. They will adapt pro formas, recalibrate underwriting, and stay hyper-local in their strategies. The era of generic national rule-of-thumb underwriting is fading.

In 2026, execution becomes the differentiator. The teams who understand how to maneuver through shifting material costs, local labor dynamics, and tariff-driven supply chains will win deals others walk away from.

Where We Go From Here

If tariffs remain in place or expand, Q1 and Q2 2026 will stay choppy. December and early-year indicators will tell us whether we get stabilization or further stress in smaller and mid-size projects.

But this market rewards clarity.

And the clarity is this: construction is walking a tightrope, and the margin for error is thin.

Developers, investors, and contractors who stay flexible — who underwrite cleanly, negotiate proactively, and localize execution strategies — will find opportunity in the volatility.

Those who rely on the previous cycle’s assumptions will find 2026 far tougher than it needs to be.