The January CCRSI data from CoStar is out and it’s telling a story the mainstream CRE press is largely getting wrong.

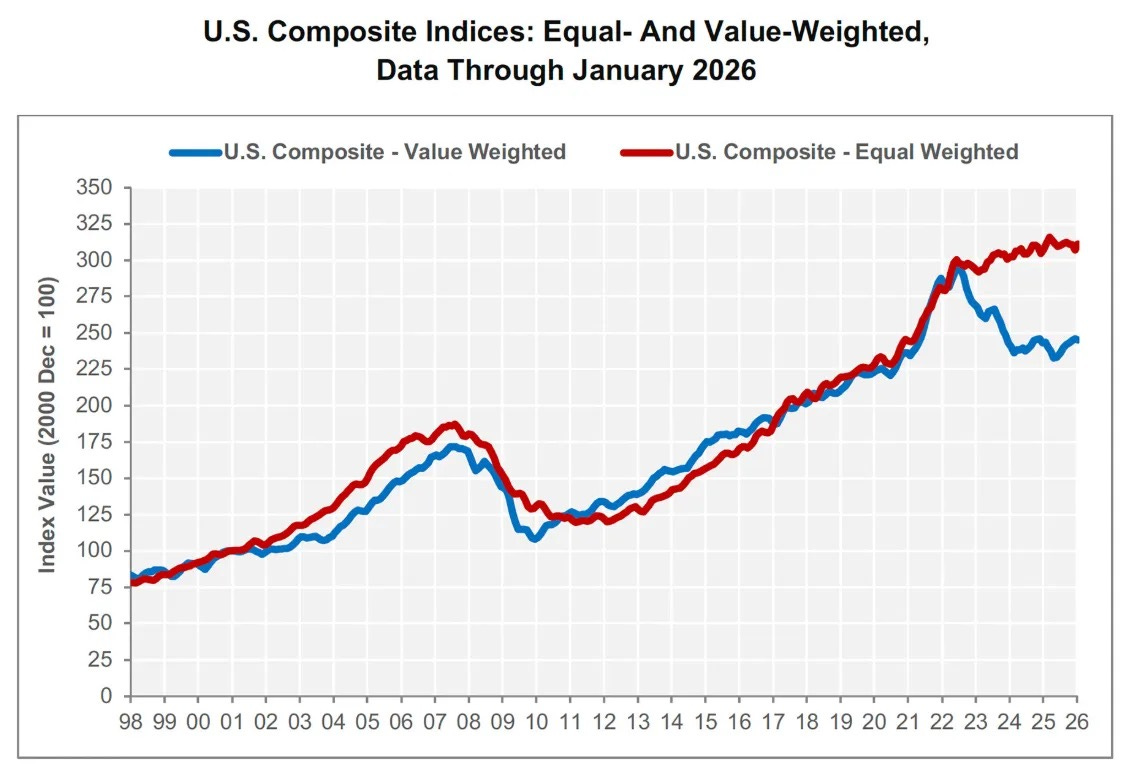

Here’s what the numbers actually say: small-market, lower-priced commercial assets are quietly gaining ground while the big-city trophy properties that dominate the headlines continue to slide. CoStar’s equal-weighted index — the one that tracks the kinds of deals I’m doing in places like Maine, Vermont, Indianapolis, Kansas City, and secondary California markets — was up 1.3% month over month and 1.1% year over year. Meanwhile, the value-weighted index, which reflects the high-end metro assets that institutional money chases, dropped 0.4% in January. It’s still 17% below its July 2022 peak and climbing back at a crawl.

January was the fourth consecutive month these two indices moved in opposite directions. That’s not noise. That’s a trend.

Why This Is Happening

Capital doesn’t disappear — it repositions. What we’re seeing right now is yield-focused buyers rotating out of overpriced gateway markets and into secondary and tertiary assets where the math still works. I’ve watched this play out on the ground across the markets I operate in. The workforce housing projects we’re building through Oldivai in places like Kansas City and Indianapolis, the mixed-use work in Vermont and Raleigh, the multifamily and co-living pipeline in Los Angeles and San Francisco — these are the kinds of plays that look smarter every quarter this divergence holds.

Big city office, Class A retail, high-end urban multifamily — all of it is still getting repriced downward as cap rates adjust to a rate environment that isn’t going back to 2021. Sellers in those markets are either capitulating or pulling listings. Withdrawal rates hit 27.1% in January. The price-to-ask ratio slipped to 92.5%. Buyers are grinding sellers down and sellers know it.

The Volume Story Is More Complicated Than It Looks

Trailing 12-month sales volume hit $146.8 billion in January, up 20% year over year. Sounds like a recovery. But look closer: repeat-sale transactions in January totaled $9.2 billion across 1,298 deals — down 10.4% from a year ago, with 143 fewer deals closing. Average days on market barely budged at 174.

The 20% volume headline is real, but it’s being driven by smaller, lower-basis transactions clearing — not a broad market reopening. The bid-ask spread hasn’t fully closed in the institutional tier. Sidelined capital is still on the sidelines, waiting for either a rate cut or enough distress to justify pulling the trigger.

The Fed is expected to cut one to three times in 2026. If that happens, liquidity comes back. But I’ve been in this business long enough to know that “expected Fed cuts” have a way of not arriving on schedule.

What I’m Watching

The deals getting done right now are the deals that made sense before the rate environment became everyone’s excuse not to move. Workforce housing in supply-constrained markets like Maine and Vermont. Mixed-use in cities with real demand drivers — Raleigh, Indianapolis, Buffalo — not just amenity speculation. Hospitality and resort assets in mountain communities where the income story holds up at current financing costs. Data center and AI infrastructure plays in markets like Virginia and Los Angeles where the fundamentals are being rewritten by a demand curve that doesn’t care about Fed policy.

If you’re waiting for the big-city market to stabilize before you deploy, you may be waiting a long time. The action has moved to secondary markets, smaller assets, and operators who know how to make the numbers work without a 2021 cap rate. January’s data is just confirmation.

— Daniel Kaufman, The Kaufman Report