Regulators may be quietly handing banks permission to get back in the game.

U.S. bank regulators have proposed easing capital requirements in a move that, if finalized, could materially shift how commercial real estate gets financed. The proposal is under a 90-day review — which means nothing is locked in — but the direction of travel is meaningful enough that operators and investors should be paying attention now.

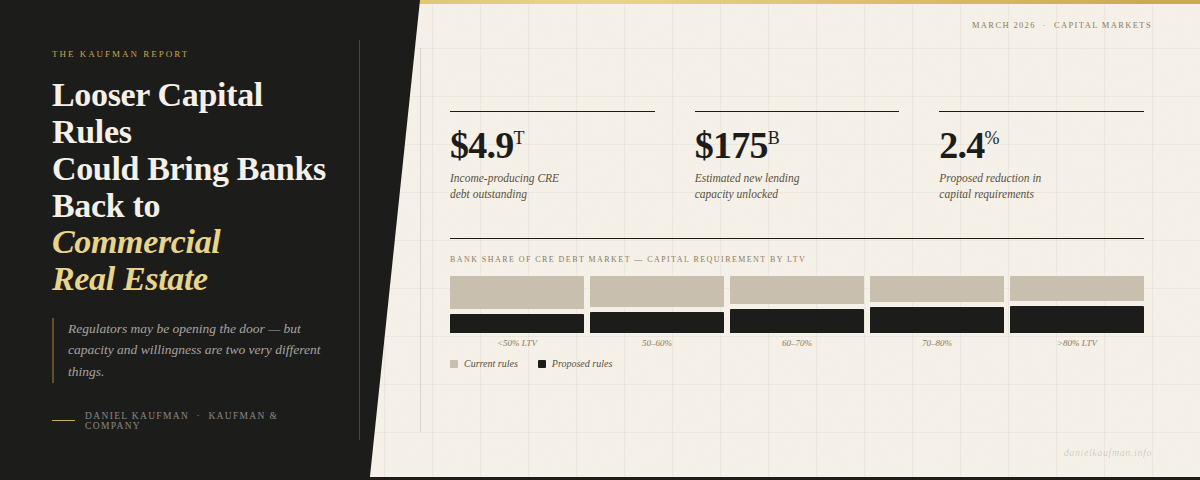

Here’s the context: banks control a significant chunk of the commercial real estate debt stack. They hold over a third of the $4.9T income-producing commercial real estate debt market, and roughly half of the $6.1T commercial mortgage market. That’s enormous. And for the past few years, regulatory pressure and balance sheet caution have kept many of them on the sidelines, particularly for anything with complexity or leverage. Non-banks — debt funds, bridge lenders, mortgage REITs — have stepped in to fill the void, and they’ve priced accordingly.

The proposed changes could cut required capital ratios by approximately 2.4%, which analysts estimate could unlock around $175B in new lending capacity. That’s not a rounding error.

The LTV shift matters

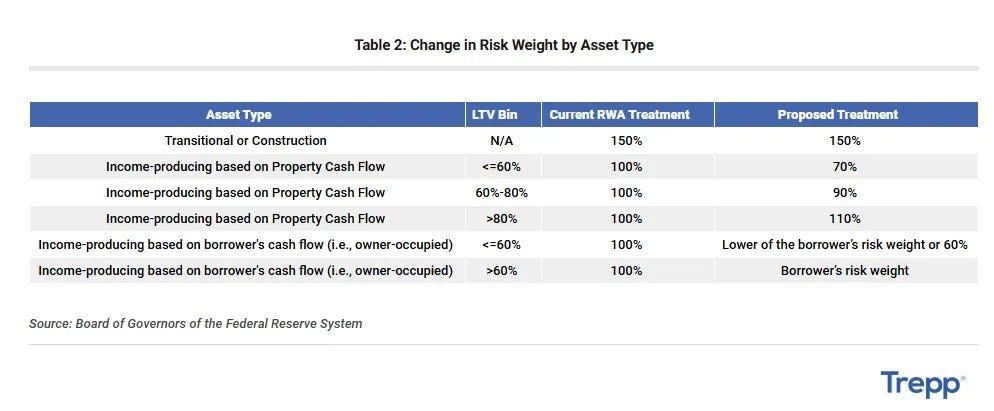

The most substantive piece of the proposal is a restructuring of how commercial real estate loan risk weights are calculated. Right now, risk weighting is applied broadly by asset category — blunt instrument stuff. The proposed framework would tie risk weights to loan-to-value ratios instead. Lower-leverage assets get lower capital charges. Higher-leverage deals carry more.

In practice, this is a meaningful shift for stabilized, well-capitalized assets. If you’re bringing a core or core-plus deal to a bank with a 55% or 60% LTV, the capital math gets a lot more favorable for the lender — which should translate into tighter spreads and more competitive pricing for the borrower.

For value-add, transitional, or construction deals? Non-banks are still going to own that space. The economics won’t change enough to bring banks back to higher-risk basis lending in a meaningful way.

Don’t get ahead of yourself

Capital relief doesn’t automatically equal lending appetite. Banks that have spent the last two years quietly managing commercial real estate concentration risk aren’t going to flip a switch because regulators loosened a ratio. Risk committees, internal concentration limits, and institutional memory of the office and retail pain still matter. Capacity and willingness are different things.

What this creates is optionality — for banks to gradually re-enter lower-leverage commercial real estate where they can underwrite cleanly, and for borrowers to potentially see better terms on the institutional-quality end of the market.

What I’m watching

Three things will tell me whether this actually moves the needle:

1. Whether the capital relief survives the 90-day review intact, or gets walked back under industry pushback

2. How the final risk weight schedule actually breaks down by LTV tier — the details here will determine whether this is meaningful or marginal

3. Whether spreads start tightening on stabilized product as banks compete for the better-basis deals

If this goes through as proposed, the structural beneficiaries are borrowers with quality, lower-leverage assets who’ve been paying non-bank pricing for bank-quality risk. That arbitrage closes. And for everyone operating in the transitional and value-add space, it’s mostly business as usual — but with a little less competition from debt funds on the safe end of the risk spectrum.

The macro tailwind for commercial real estate debt availability is real. Whether it’s a wave or a ripple depends entirely on implementation.

The Kaufman Report covers real estate capital markets, development, and investment from an operator’s perspective. Subscribe for weekly analysis.