There’s a gap forming in commercial real estate right now. Not a gap in fundamentals. Not a gap in transaction activity. A gap between what the data says and what the sentiment says — and if you’ve been doing this long enough, you know exactly what that gap means.

It means we’re early.

Private Credit Had a Great Run. Now It’s Fading.

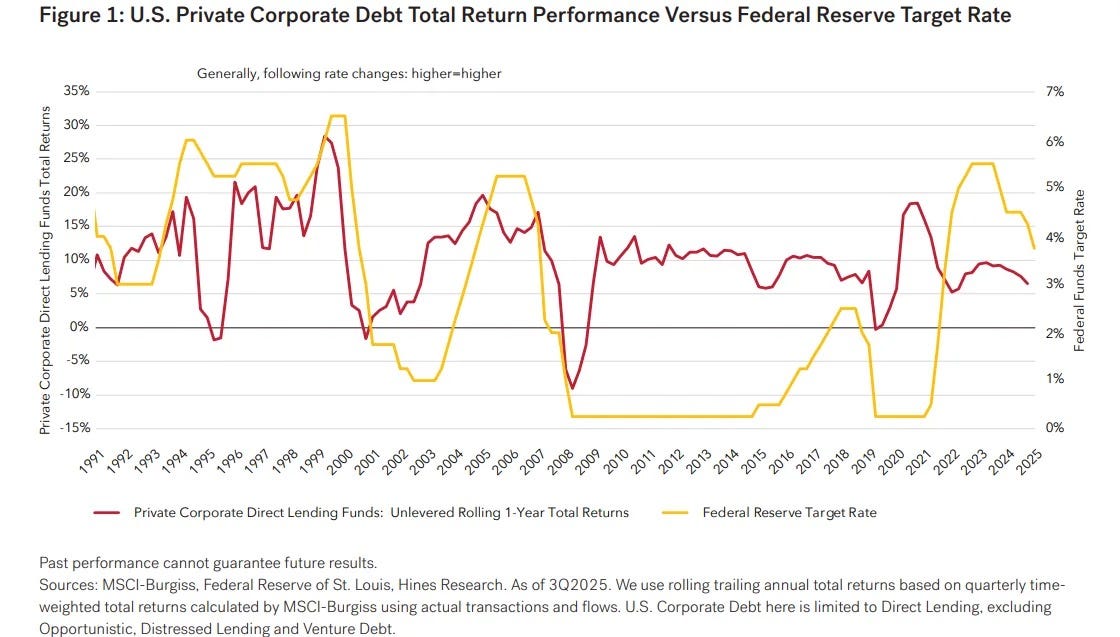

Private corporate debt has been a portfolio workhorse for the better part of three years. Twenty-two of twenty-three consecutive quarters in positive territory. Nine-plus percent annualized returns. Floating-rate income doing exactly what it was supposed to do in the rate environment that built it.

That environment is ending.

Three consecutive Fed cuts totaling 75 basis points in the back half of 2025 are compressing floating-rate yields and normalizing the premium that made private credit so compelling. This isn’t a collapse — it’s a rotation signal. And the allocators paying attention are already moving.

$1.3 Trillion. That’s the Gap.

Here’s the number that should be anchoring every capital allocation conversation right now: $1.3 trillion. That’s the annual global investment shortfall across housing, energy, and infrastructure — the delta between what public balance sheets can fund and what actually needs to get built.

Government isn’t closing that gap. Private real estate does.

And unlike the rate-sensitive yields that powered private credit through the last cycle, real estate cash flows are anchored in rents and occupancy — durable, tax-advantaged income that doesn’t require a specific monetary policy environment to perform. Over the last two decades, more than 80% of core real estate returns came from income. That’s not a pitch. That’s the asset class doing what it’s always done.

The Data Is Already Moving — Sentiment Just Hasn’t Caught Up

Here’s where it gets interesting for operators who actually track the numbers.

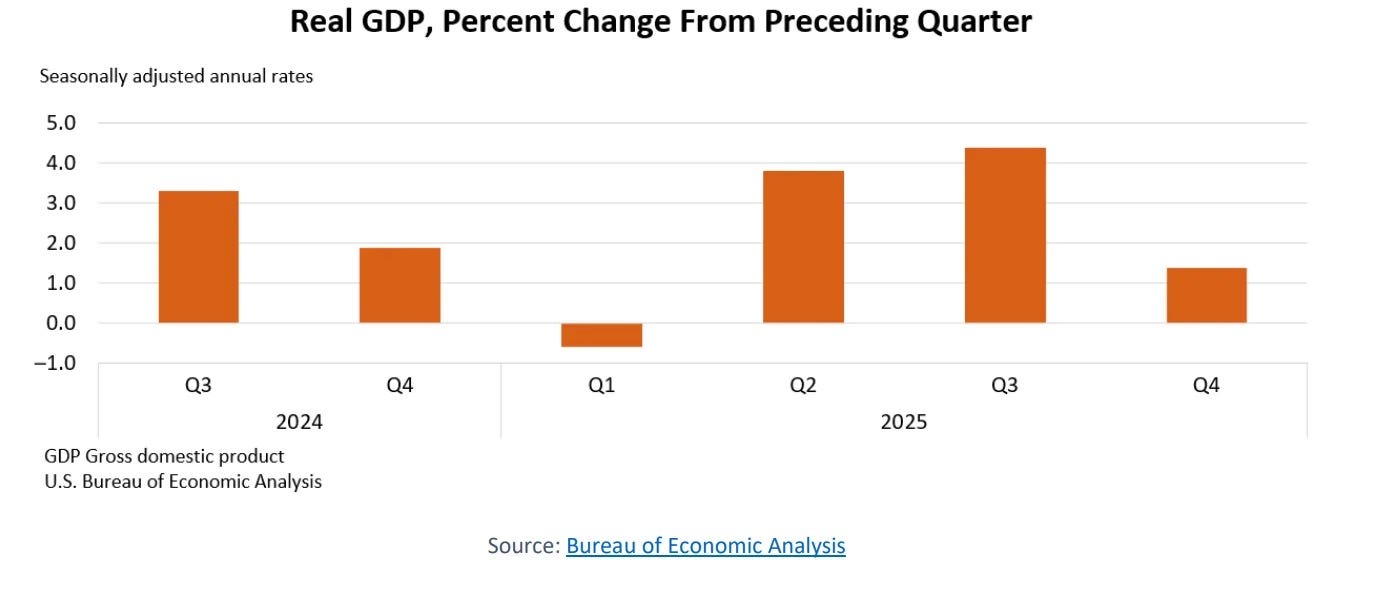

Real GDP grew 2.2% in 2025. Inflation moderated to 2.4%. Unemployment held near historic lows at 4.3%. The macroeconomic foundation that drives real estate demand — employment, income growth, business formation — is intact. Yet sentiment in commercial real estate remains cautious. That divergence is the opportunity.

Total US CRE investment volume rose 22% year over year in 2025, reaching $499 billion. Q4 alone jumped 29% to $172 billion. Meanwhile, CBRE’s Lending Momentum Index climbed to 1.2 — its highest reading since 2018 — signaling that risk appetite is returning to credit markets in a meaningful way. Liquidity is coming back. Transaction volume is accelerating. And asset valuations have reset to some of the most attractive entry points in over a decade.

This is not a rumor. This is the data.

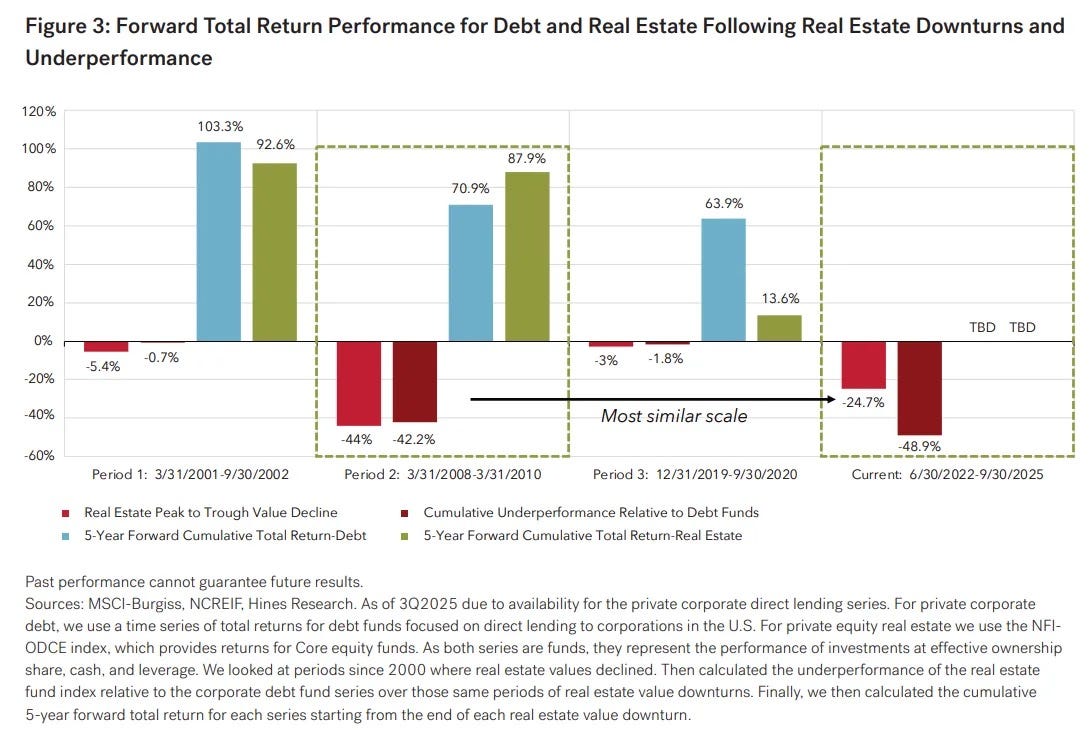

The Underperformance Gap Is the Setup

Since mid-2022, private real estate has underperformed private corporate debt by nearly 49%. To the uninformed, that looks like a reason to stay away. To anyone who’s studied cycle history, that’s the setup.

The three prior comparable downturns each saw real estate outperform by roughly 20% over the subsequent five years. And we’re not waiting on a lagging indicator here — core real estate indices have already posted six consecutive quarters of positive returns after what increasingly looks like the cycle bottom. The recovery isn’t hypothetical. It’s already underway.

Capital is confirming it. The largest non-traded equity REITs raised 36% more in the first three quarters of 2025 than the same period a year prior. More telling: net flows flipped from -$677 million to +$436 million — a $1.1 billion swing in institutional conviction. When that kind of money moves before the mainstream narrative catches up, it’s worth paying attention.

Where the Opportunity Is Concentrated

Not all of CRE is created equal coming out of this reset.

Multifamily is leading the recovery, capturing the largest share of investment activity as capital returns to the sector and fundamentals stabilize. Across asset types, the lending environment has grown more disciplined — financing is flowing to strong sponsors with well-performing assets, while less resilient deals face restructuring or distressed sales at reset valuations. That bifurcation is exactly the environment where experienced operators with sound capital structures pull away from the pack.

A looming wave of loan maturities is creating additional opportunity for well-capitalized investors as price discovery resumes and distressed assets surface at compressed valuations. The market is shifting from multiple expansion to a focus on operational income and rigorous asset management — which, frankly, is where it always should have been.

The Playbook

This isn’t a call to abandon private credit. Durable income still belongs in any serious portfolio. The call is to pair that income with real estate exposure at a valuation that hasn’t looked this attractive in years — and to do it before the sentiment catches up to the data.

The investors who outperform coming out of a reset don’t wait for consensus. They look at transaction volume, lending momentum, capital flow data, and macroeconomic fundamentals — and they move while the narrative is still cautious.

The sentiment gap is real. The fundamentals are stronger than the headlines suggest. And the window to position ahead of the recovery cycle is open.

It won’t stay that way.

Daniel Kaufman is the Principal & CEO of Kaufman & Company, a Los Angeles-based real estate investment and development firm. Views expressed are his own.