Oracle laid off 30,000 people last week. OpenAI raised $122 billion. Neither of these is good news.

Let’s start with Oracle.

Thirty thousand workers. Gone. That’s roughly 18% of their global workforce, accounting for about $8 billion a year in salaries. Simultaneously, Oracle announced it would invest $50 billion — this year alone — in AI infrastructure.

Do the math. That’s not a restructuring. That’s a statement.

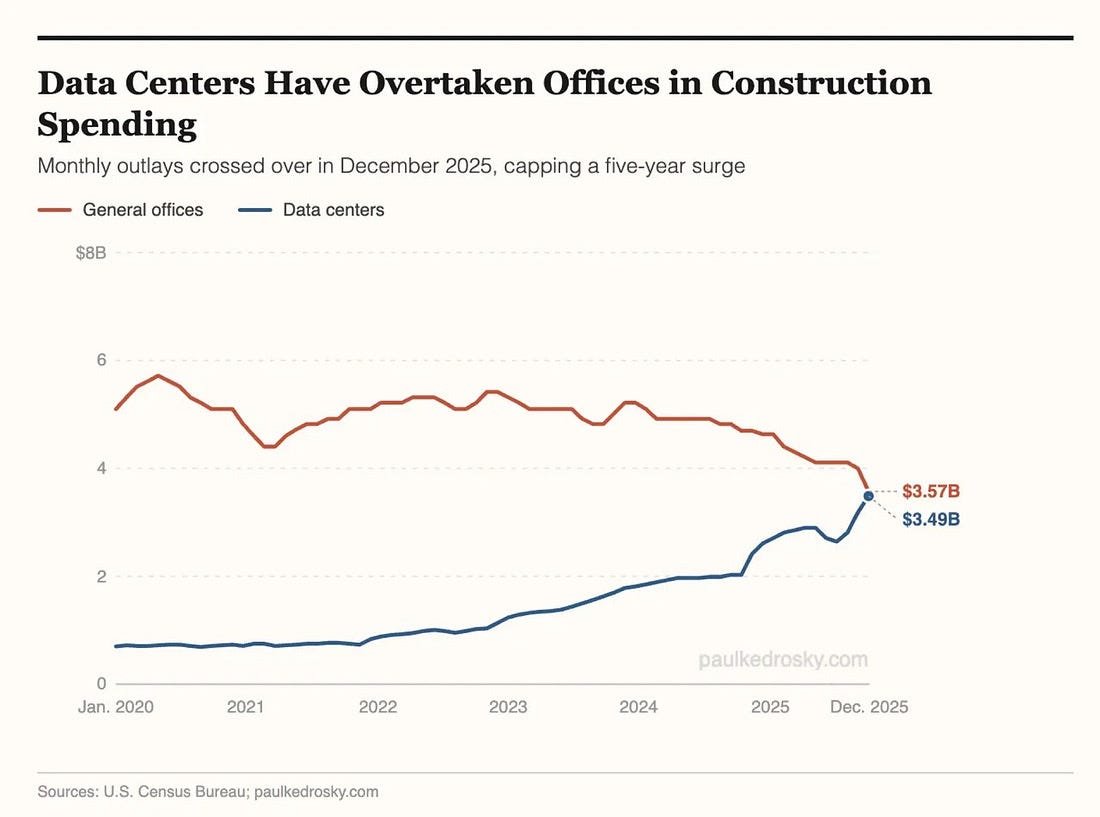

For the first time in modern history, the amount of capital flowing into data center construction has surpassed what’s being spent on office buildings. Think about what that means. The physical infrastructure of the 21st century economy isn’t cubicles and conference rooms anymore. It’s server farms. Cooling systems. Fiber. Power.

The server farm is the new human.

And if you think Oracle is some outlier here — you’re not paying attention. This is the playbook every major enterprise tech company is running right now. Fewer salaries. More kilowatts. Layoffs aren’t a sign of a struggling business. They’re increasingly the hallmark of a company that thinks it’s figured something out.

Now let’s talk about OpenAI.

Last week they announced a raise of $122 billion at an $852 billion valuation — the largest private fundraise in history. The headlines were rapturous. A vote of confidence in AI! The future is here!

Dig one layer deeper.

Of that $122 billion, $110 billion came from exactly three companies: Amazon ($50B), Nvidia ($30B), and SoftBank ($30B). These aren’t arms-length investors making a cold bet on OpenAI’s prospects. These are deeply entrenched strategic partners who need OpenAI to succeed because their own businesses are built on top of it.

There’s an old joke in business: If I owe you a million dollars, I’m in trouble. If I owe you a billion dollars… you’re in trouble.

Microsoft, Nvidia, and SoftBank are so far in hock to OpenAI that they functionally can’t let it fail. That changes the calculus on what this “fundraise” actually signals.

The remaining $12 billion? That came from everyone else — including Microsoft, which has already committed billions. So the actual new outside money here is a rounding error on an $852 billion valuation.

Meanwhile, OpenAI quietly pulled the plug on Sora.

Remember Sora? The AI video product they launched with enormous fanfare, complete with high-profile Disney partnerships and breathless press coverage? The one that was supposed to transform content creation?

Gone. The computing costs alone were running north of a million dollars a day. Demand didn’t justify the burn. So they killed it.

What did they do instead? They acquired TBPN — the YouTube and X show — for hundreds of millions of dollars.

TBPN, for what it’s worth, is a show I appeared on a few months ago to talk about Noble Mobile. It’s a solid tech media property. But why is an AI company spending hundreds of millions to buy a media channel?

The cynical answer — and I think the correct one — is narrative control. When your stock is valued at $852 billion and your enterprise sales are still a work in progress, you need the tech commentariat on your side. Owning the microphone is cheaper than changing the fundamentals.

It’s not a normal business move. It raises more questions than it answers. But when you can spend $200 million and it barely registers as a footnote on your cap table, why not?

On the revenue side, OpenAI posted $2 billion a month. ChatGPT dominates consumer AI. But the enterprise market — where the real money is — remains contested.

Their most credible competitor, Anthropic, is preparing to go public in what could be one of the largest IPOs in recent memory. The people I talk to use “Claude” the way a previous generation used “Google” — as a verb, as a default, as the tool you reach for when you need to actually get something done in a professional context. That’s the market OpenAI is chasing.

So what do I take away from all of this?

First: The scale of AI infrastructure investment has officially crossed into territory where human labor is just a line item to be optimized away. Data centers are the new offices. The layoffs we’re seeing aren’t economic distress — they’re strategic repositioning. Expect more.

Second: For OpenAI to justify $852 billion, it needs to generate tens of billions in additional annual revenue. That math only works if it displaces a massive share of the knowledge workforce, captures enterprise at scale, or — most likely — fails to hit its projections and goes through a painful repricing. Maybe all three.

Third: OpenAI has become too big to fail. The banks learned what that status costs during the mortgage meltdown — it ends with the federal government as backstop. If OpenAI ever needs that kind of intervention, the market disruption that follows will make 2008 look orderly.

None of this is good news.

The people being counted as costs to be eliminated are real. The capital being deployed is real. The disruption is real and accelerating.

Prepare accordingly.

The Kaufman Report is published , Principal & CEO of Kaufman & Company. Views are his own.