The pipeline has been cut nearly in half. That’s not a crisis for retail landlords — it’s an accidental moat.

The headlines keep calling retail dead. The supply data is telling a completely different story.

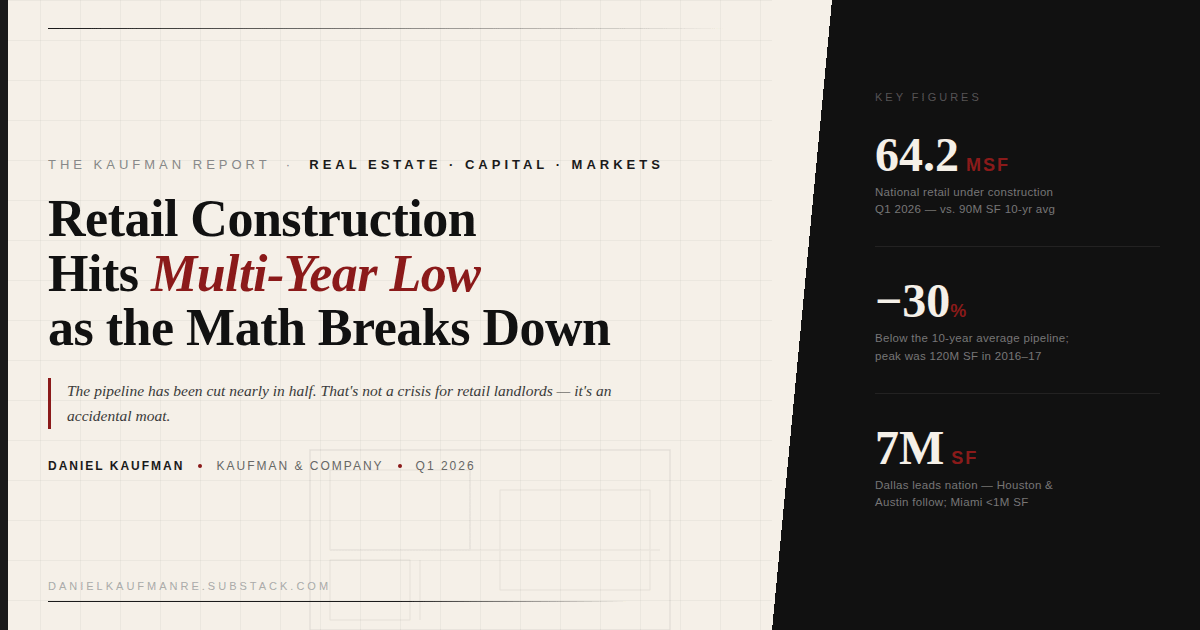

Only 64.2 million square feet of retail was under construction nationally in Q1 2026. That’s down 8% from a year ago, and roughly 30% below the 10-year average of 90 million SF. At the peak — 2016, 2017 — you had 120 million SF in the pipeline. That number has been cut nearly in half in under a decade.

Why Developers Aren’t Building

I’m a developer. I can tell you exactly why the math doesn’t work right now.

Land costs are up. Hard costs are up. Capital is expensive. And the rents you’d need to clear a reasonable return on ground-up retail construction are well above what most tenants are willing to pay — even in markets with real population growth and strong leasing demand. CoStar’s national director of retail analytics Brandon Svec put it plainly: achieving returns that justify ground-up construction has become “increasingly challenging.”

That’s a polite way of saying most projects don’t pencil.

This isn’t a sentiment problem or a demand problem. It’s a cost-stack problem with no obvious near-term solution. The gap between what developers need to charge and what tenants will absorb has widened to the point where the math simply stops working in most markets.

Where Development Is Still Happening

Texas is carrying the country — and doing it right.

Dallas led all markets with nearly 7 million SF under construction in Q1. Houston followed at just under 4 million SF. Austin came in at just over 3 million SF. The majority of that Texas pipeline was pre-leased before a shovel hit the ground. That’s disciplined, build-to-suit development in the right markets — not speculative retail chasing yield.

Miami, for comparison, had less than 1 million SF underway. That number says everything.

The Macro Overlay Isn’t Helping

The development environment was already constrained. The macro picture is making it worse.

Tariffs, Iran-driven energy volatility, and a cautious consumer are layering on top of an already difficult construction market. The two-week ceasefire announced this week may take a few cents off gas prices in the near term, but Tehran still controls the Strait of Hormuz — and the 10% baseline import tariffs remain in place, currently facing legal challenges from 21 states. This environment isn’t clearing up in any meaningful timeframe.

When you combine elevated construction costs, expensive debt, tariff uncertainty, and softening consumer confidence, you’re not looking at a temporary pause in retail development. You’re looking at a structural reset in what gets built, where, and by whom.

The Part Most People Miss

Here’s where the conventional wisdom gets it wrong.

The retail industry’s supply problem is quietly becoming its most durable structural advantage. When you can’t build new product — and right now, you largely can’t — the well-located existing retail you already own becomes something close to a moat.

With construction running 30% below the long-run average and the development math showing no signs of improvement, existing quality retail is becoming scarcer by default. Landlords sitting on well-located assets in supply-constrained markets are entering a period of pricing power that the headline narrative on retail has consistently underpriced — not because they were visionary, but because the pipeline dried up and nobody’s replacing what they have.

The “retail is dead” narrative has been wrong for years. The supply math is making it even more wrong going forward.

The story isn’t that retail is dying. The story is that the product replacing it is barely being built.

The Takeaway

New retail space was already hard to find. It’s about to get harder.

Retail construction is running at 64.2M SF nationally — 30% below the 10-year average, and nearly half the peak levels of 2016–17. The cost stack has broken the development equation in most markets. Texas is the exception. The rest of the country is watching its retail pipeline quietly evaporate.

For owners of quality, well-located existing retail: this is the supply story working in your favor. You don’t have to like the macro environment to understand what it means for your position.

The Kaufman Report is published , Principal & CEO of Kaufman & Company. Views are the author’s own based on market data and 25+ years of operator experience.

About the Author

Daniel Kaufman is the Principal and CEO of Kaufman & Company, a Los Angeles-based real estate development and investment firm with over 25 years of experience across multifamily, mixed-use, workforce housing, resort, and industrial development — including emerging sectors like AI-driven micro data centers.

Daniel has spent his career operating across the full capital stack — as a developer, investor, and lender — with active projects spanning California, Vermont, Maine, the Sun Belt, and the Midwest. He is the founder of Convivium Living, a multifamily lending and investment platform, and Oldivai, a modular construction and workforce housing development vehicle.

His investment thesis is consistently contrarian and data-grounded: secondary and tertiary markets over gateway cities, workforce product over luxury, and supply dynamics over sentiment. He has been publicly bullish on Chicago when others called it a doom loop, skeptical of Florida at the top, and early on the data center opportunity before it became consensus.

The Kaufman Report is his platform for operator-perspective analysis on real estate markets, capital, and development — written for people who are actually in the business.

Subscribe at danielkaufmanre.substack.com

Follow on Instagram · Twitter/X (@realdanielkaufman)

Company: thekaufmanco.com