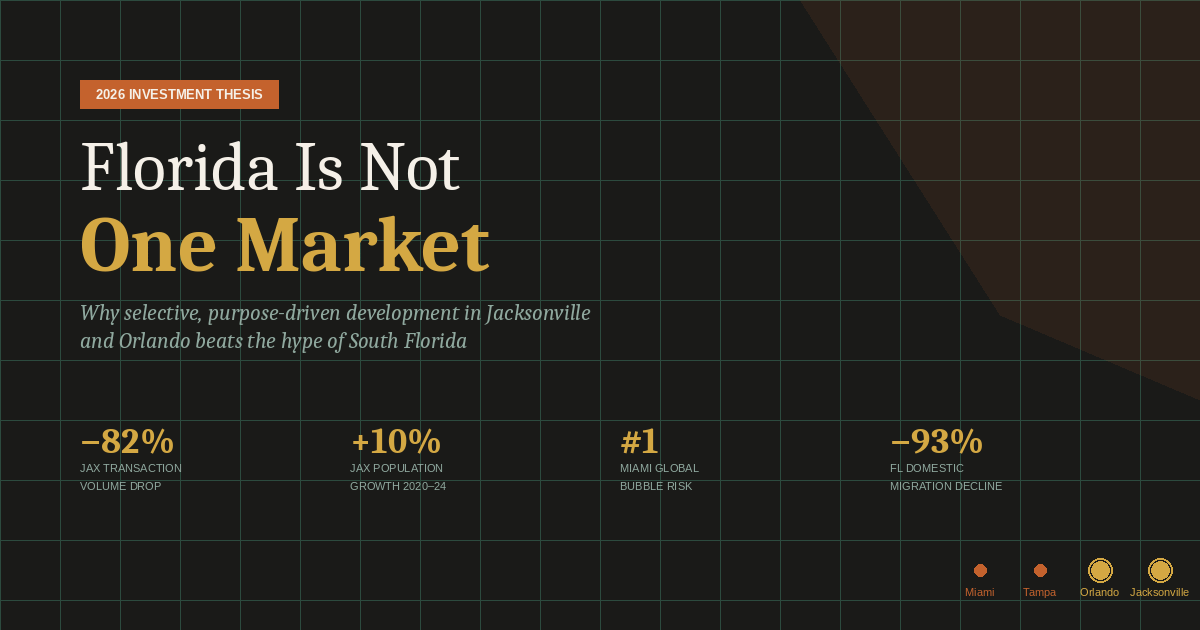

The narrative around Florida real estate tends to flatten everything into one story: sunshine, migration, opportunity. But that’s a dangerous oversimplification for anyone deploying capital. Florida in 2026 is a tale of diverging markets, and the investors who understand the difference between them will be the ones who build lasting value. Those who don’t will be buying into a story that the data no longer supports.

I’ve spent the better part of this month repositioning around two markets I believe in, Jacksonville and Orlando, while deliberately staying away from the noise of Miami, Tampa, and the broader South Florida corridor. Here’s why.

The Case for Jacksonville: Undersupplied, Undervalued, and Underestimated

Jacksonville is the sleeper city of the Southeast, and that window is closing.

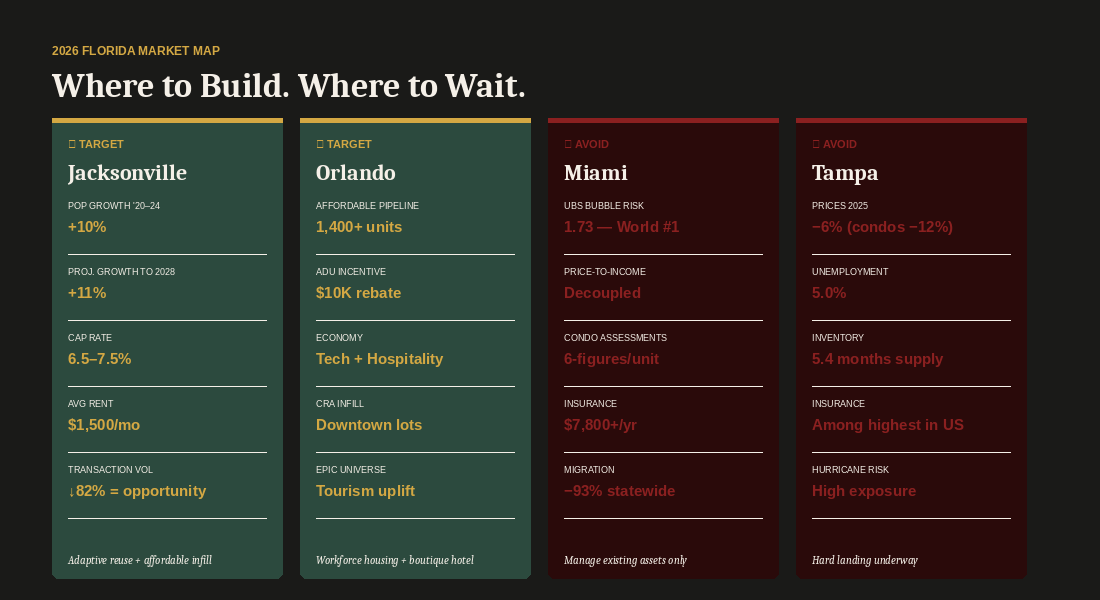

The fundamentals are stacking up in a way we rarely see aligned this cleanly. The population of the Jacksonville metro area grew nearly 10 percent between 2020 and 2024, driven by the strongest employment growth in Florida, and the Wall Street Journal and Moody’s Analytics ranked it the second strongest job market in the nation. From 2023 to 2028, Jacksonville is projected to grow by 11%, faster than any other major Florida metro, the state average, and the country as a whole.

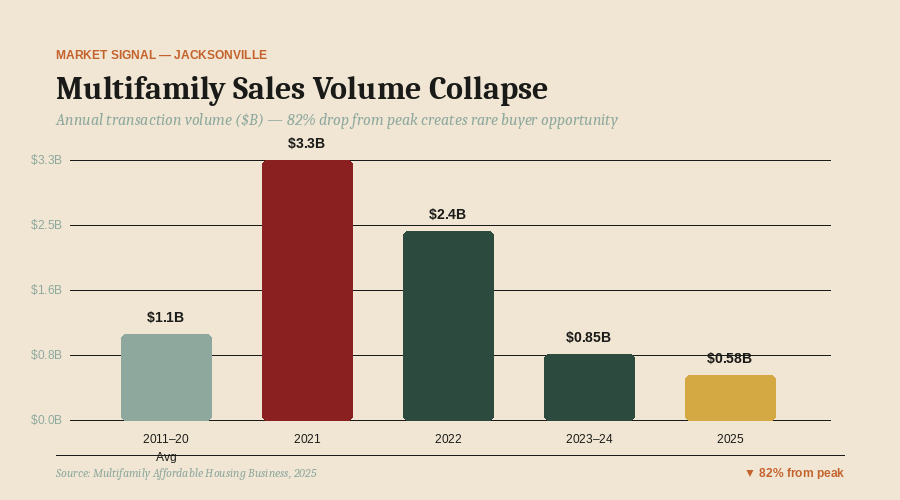

Meanwhile, the transaction market has been in a deep freeze. Annual multifamily sales volume dropped from a peak of $3.3 billion in 2021 to just $584 million as of late 2025 — a decline of over 80%. Same-store prices are still roughly 19% off their 2022 peak. This is precisely the kind of market dislocation that creates opportunity for developers and operators willing to move when others are sitting on their hands.

What makes this moment particularly interesting is the supply picture. After a construction surge that added 33,557 units — a 26% increase to total inventory — between 2020 and 2025, new starts have collapsed back to normalized levels. The pipeline is thinning. Demand, meanwhile, keeps coming: over 100 new residents a day are arriving in Northeast Florida, according to the U.S. Census Bureau.

The institutional capital that overbuilt during the pandemic era is now under pressure to exit. Lenders and capital partners are beginning to push sellers who have been holding beyond their intended exit windows. That pressure creates motivated sellers and real pricing discovery — exactly the environment where disciplined acquirers and adaptive reuse developers can execute.

What We’re Doing There

We are currently kicking off an adaptive reuse project in Jacksonville — converting a former factory into apartments. This type of conversion checks every box for the current moment: lower land cost than ground-up, character and authenticity that the market rewards, and a faster path to stabilization. The city’s downtown has seen a remarkable pipeline of similar projects take shape, from JWB Real Estate Capital’s conversion of the First Baptist Convention Building into mixed-use apartments and restaurants, to the $55 million Corner Lot Development Group project repurposing the city’s first Chevrolet dealership.

We are also developing new affordable housing on an urban infill site, similar in spirit to the Oldivai Project Zero model — small-scale, community-integrated, purpose-built for the workforce that is actually arriving in the city. Jacksonville’s diverse economy — logistics, healthcare, financial services, military, manufacturing — produces exactly the kind of essential workforce that needs this product. These aren’t abstract buyers. They’re here, they’re employed, and the city is not building fast enough to house them at attainable price points.

The University of Florida is also constructing a $300 million graduate campus in downtown Jacksonville set to open in 2026. The Jacksonville Jaguars are executing a $1.4 billion stadium renovation. These aren’t vanity projects. They are the kind of institutional anchors that drive residential and hospitality demand for years.

Cap rates in Jacksonville’s multifamily market are currently running between 6.5% and 7.5% — among the most attractive in Florida — while rents are averaging around $1,500/month with a 6.3% vacancy rate. For developers who can control cost basis, this is a workable spread.

The Case for Orlando: Undersupplied Workforce Housing in a City That Keeps Growing

Orlando gets a lot of press as a theme park economy. The reality is more interesting. The city has been quietly diversifying — into simulation technology, health tech, aerospace, and logistics — while its housing affordability crisis has become acute.

We have reopened our office in Orlando’s downtown and are actively looking at small-scale urban infill opportunities in affordable housing, workforce housing, and hospitality. The rationale is straightforward:

Demand for workforce and affordable housing is structural and growing. Nearly 1,400 new units — including over 1,000 designated affordable — are under development to meet the gap, but supply remains far behind need. The City of Orlando’s Community Redevelopment Agency is actively moving vacant lots in the Downtown CRA into owner-occupied and affordable product. The city recently approved an incentive program paying homeowners up to $10,000 to build and rent accessory dwelling units as workforce housing, signaling that even the smallest scale of housing production is being encouraged.

The hospitality angle in Orlando is also compelling — particularly for boutique, experience-driven product. Universal’s Epic Universe expansion is expected to drive a meaningful step-up in tourism and the hospitality labor pool that supports it. There is a genuine gap in the mid-market and boutique hospitality segment that larger institutional capital won’t touch.

Small urban infill is not glamorous. It doesn’t generate press releases or attract the sovereign wealth funds. But it produces durable returns, serves a real and growing community need, and in a market like Orlando’s downtown, it benefits from city-level tailwinds that are only getting stronger.

Why I’m Staying Away from Miami and Tampa

Let me be direct about this, because I think a lot of capital is still being drawn to these markets by reputation rather than current fundamentals.

Miami is the most overvalued housing market in the world right now, according to UBS’s 2025 Global Real Estate Bubble Index — scoring 1.73, well above the 1.5 “high risk” threshold and exceeding even the peak of the 2006 bubble. Price-to-rent and price-to-income ratios have decoupled from fundamentals. The luxury condo market is facing a convergence of deferred structural maintenance, rising HOA assessments, surging insurance costs, and the downstream fallout from Florida’s condo safety laws passed after the Surfside collapse. Many older buildings are staring at special assessments in the six figures per unit.

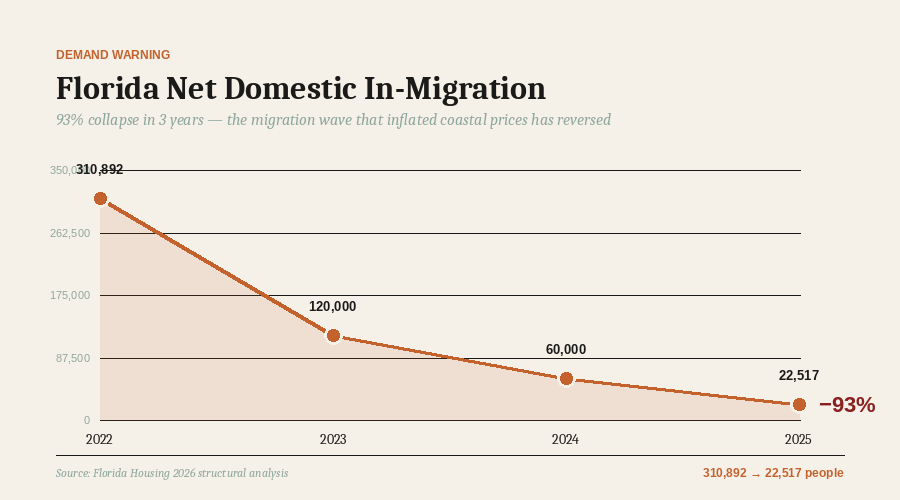

Net domestic migration into Florida fell from 310,892 in 2022 to roughly 22,517 in 2025 — a 93% decline — driven almost entirely by the cost and insurance crisis in the state’s coastal metros. The buyers who once showed up with cash from New York and California are not arriving at the same rate, and the local demand pool cannot support the price levels that remain in place.

Tampa is experiencing the same structural pain with a harder landing. Home prices fell 6% in 2025 and are expected to continue declining. The condo and townhome segment dropped 12%. Tampa hit 5.0% unemployment by late 2025. Inventory is up nearly 15% year-over-year with a 5.4-month supply. Insurance premiums are among the highest in the country, and repeated hurricane seasons have made flood risk a first-order concern for buyers in ways it simply wasn’t a decade ago.

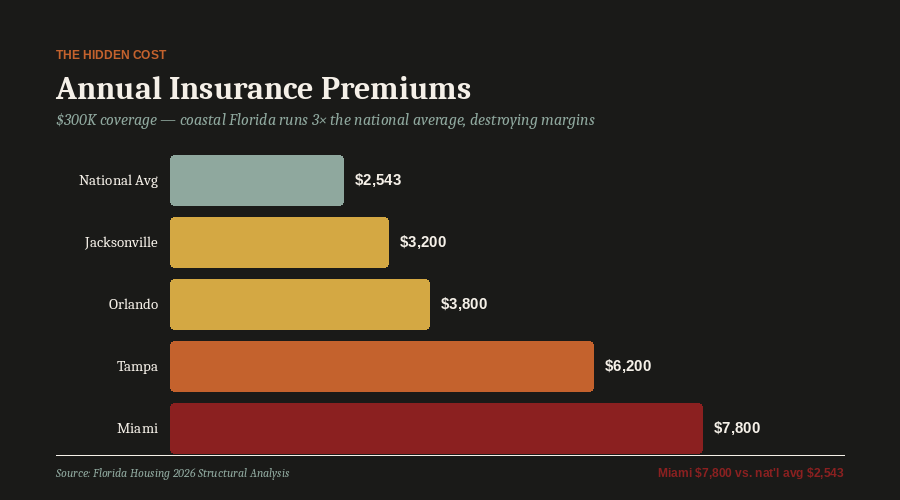

Statewide, Florida insurance premiums average $7,136 for $300,000 in coverage, compared to a national average of $2,543. That carrying cost is quietly destroying cap rates, net operating income, and the affordability math for buyers across coastal Florida. It doesn’t show up in the headline price numbers — but it shows up in operating budgets, in buyer hesitation, and in the growing number of price reductions that now account for over a third of active listings statewide.

These are not markets to avoid forever. But in 2026, with capital costs elevated and these structural headwinds fully in view, I don’t see a compelling risk-adjusted case for new development in Miami or Tampa. The story there is about managing existing assets, not creating new ones.

The Principle Behind the Strategy

The thesis here is not complicated, but it requires discipline to execute: go where the demand is real, where the supply is constrained, where the city is invested in growth, and where the asset class you’re working in solves a genuine problem.

Affordable and workforce housing in Jacksonville and Orlando is not charity work. It is the most structurally sound product category in both markets right now — driven by employment growth, supported by city policy, and insulated from the luxury volatility that has burned investors in the coastal markets.

Adaptive reuse in Jacksonville converts stranded industrial assets into housing using existing structure and character that cannot be replicated with new construction. Boutique hospitality in Orlando serves a market that the institutional players are ignoring.

Florida still has exceptional opportunity. But it is not uniformly distributed. The investors who win here in the next cycle will be the ones who read past the state-level headlines and understand that Jacksonville and Orlando are different stories than Miami and Tampa — and are different from each other.

We are building in the gap between where the capital has been and where the demand is going. That gap, right now, is large. It won’t be forever.

Daniel Kaufman is a builder, investor, and founder with over 25 years of experience in real estate development and more than $2 billion in project value delivered across residential, commercial, hospitality, and mixed-use sectors nationwide. His work spans over 1,800 units in affordable and mixed-income housing, 2,200+ units in market-rate multifamily, hotels, and office developments — always grounded in disciplined underwriting and hands-on execution from land acquisition through long-term operations.

Daniel’s development philosophy is built on a simple set of principles: strategic site selection, integrated design and construction, rigorous risk identification, and an uncompromising standard for quality. His current focus includes adaptive reuse, workforce and affordable housing, build-to-rent communities, and urban infill across high-growth markets — with active projects now underway in Jacksonville and Orlando.

Beyond development, Daniel is engaged in a range of ventures spanning modular construction, data center and AI infrastructure, and structured real estate finance — building an integrated platform that operates across asset classes and investment horizons.

Learn more at danielkaufmanre.com or connect on Instagram, LinkedIn, and X.