The past year didn’t give us the clean narrative everyone wanted. Since 2020, the real estate industry has tried to frame each year as the beginning or end of a cycle. But if you work directly in development and investment, you know the market almost never moves in straight lines. It shifts in layers. It evolves unevenly. And sometimes the signals that matter most are the ones hiding under the headlines.

As I look back on rental data from 2025, the emerging “Peak 65” demographic wave, and the broader macro resets shaping capital markets and commercial real estate, a single theme keeps surfacing: demand is not disappearing. It’s reorganizing. And the markets that understand this are the ones that will define 2026 and beyond.

What follows is how I see the landscape right now, through the lens of someone who develops, invests in, and operates real estate across multiple regions and asset classes.

1. The Rental Market Delivered a Clear Message: Supply Helps, But It Isn’t Enough

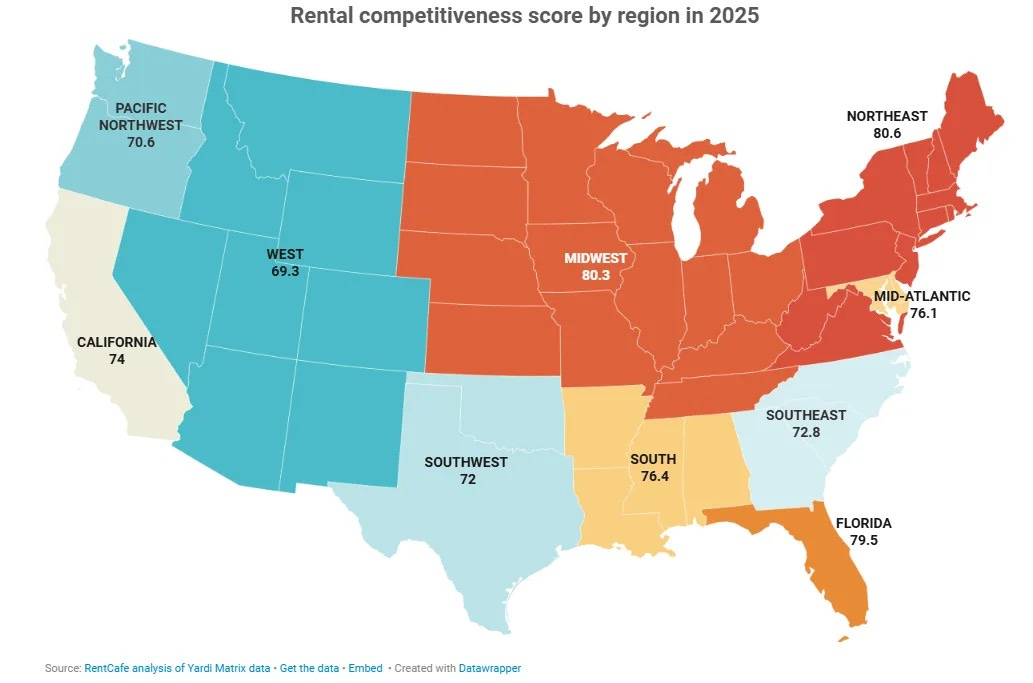

We ended 2025 with one of the most competitive rental markets in recent memory.

Even with 500,000+ new apartments delivered, the national Rental Competitiveness Index still rose. Renewal rates climbed to 63%, vacancies tightened, and the average unit drew nine renters competing for the same apartment.

The narrative that “a flood of supply will cool rent demand” simply didn’t play out. It helped, but it didn’t resolve the underlying imbalance: we aren’t building enough where people actually want to live.

Look at the metros sitting at the top of the competitiveness rankings:

Miami: 19 applicants per unit, 73% renewals, vacancies below 4%.

Chicago: Supply slowed, demand didn’t. Occupancy around 95%.

Manhattan: Return-to-office pushed renewals above 66%, occupancy near 96%.

Twin Cities suburbs: Big RCI jump driven by slowed construction and strong household formation.

Port St. Lucie: The year’s sleeper market, with a 12-point RCI surge and 75% renewals.

When renters are renewing at historic levels and new supply is being absorbed immediately, it signals something deeper than a cyclical fluctuation. It suggests we’re shifting into a structural phase where mobility decreases, household formation remains strong, and lifestyle preferences keep clustering around certain metros.

Supply will provide momentary relief early in 2026, but by midyear the gap widens again as construction slows. The cycle is becoming more predictable: short periods of cooling, followed by tightening that lasts longer than expected.

2. “Peak 65” Is Not a Retirement Story — It’s a Real Estate Story

More than 4 million Americans will turn 65 in 2026, the highest number in U.S. history. This demographic wave is going to have an impact on the built environment that rivals the Millennial housing boom.

But here’s what stands out: retirees today don’t behave like the retirees of 20 years ago.

They’re not just chasing beaches. They’re chasing stability. Strong healthcare systems. Reasonable costs. Community infrastructure. Flexibility. And increasingly, they’re navigating transitions—downsizing, relocating, aging in place—while still wanting access to the activities that define their lifestyle.

Yes, Florida still dominates the rankings. Cape Coral–Fort Myers, Naples, Sarasota, and Port St. Lucie continue to attract retirees for good reasons: longevity, climate, income levels, recreation. But rising insurance costs and home prices are creating pressure that didn’t exist a decade ago.

This is where secondary metros are stepping forward:

New York–Newark–Jersey City: High healthcare density and transit access.

Poughkeepsie: Strong safety levels, unmatched healthcare access per capita.

Madison, WI: Low crime, great air quality, tax advantages for Social Security.

Boise: Country’s safest metro, strong outdoor lifestyle, new housing geared toward aging residents.

Durham–Chapel Hill and Virginia Beach: Healthcare concentration, affordability, and community networks.

It’s not a Sun Belt vs. Rest-of-Country discussion anymore. It’s a segmentation story: different retiree profiles choosing metros that meet different needs.

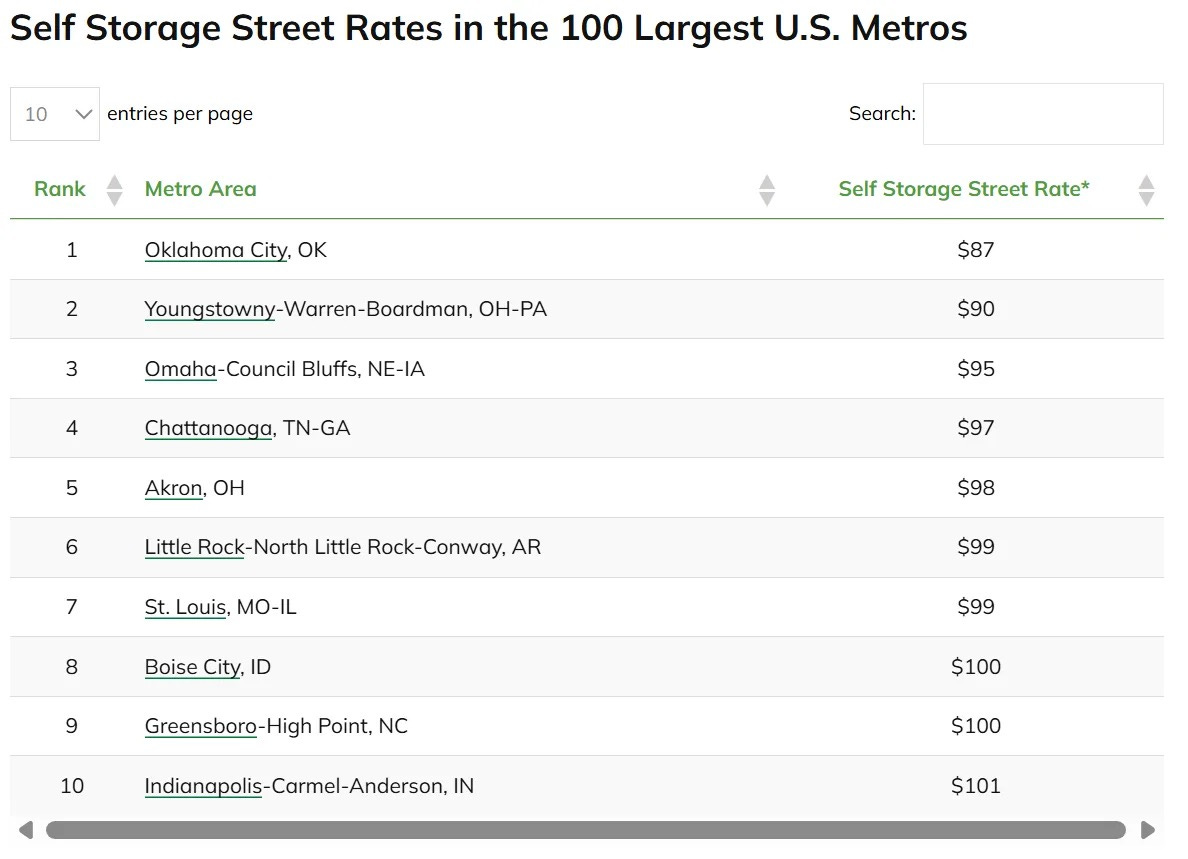

An overlooked piece of this ecosystem is self-storage. As people transition into smaller homes—or stay put and reorganize their living space—storage becomes the quiet infrastructure that enables flexibility. Boise’s average $100/month storage cost tells you everything: consumers value space, but not always inside their home.

3. The Broader Economy Is Slowing — But Real Estate Is Rebalancing, Not Retreating

The macro backdrop shifted in 2025. GDP cooled from 2.8% to 2.1%. Hiring became harder. Immigration policy and tariffs pushed costs up. And though the Fed began cutting rates, long-term yields remained stubborn.

But the conversation often misses the more important point: markets are normalizing, not collapsing.

Here’s how I see the key sectors:

Office

We’re settling into a post-pandemic equilibrium. The best buildings—well-located, hospitality-inflected, amenitized—are regaining footing. Vacancy hovering under 18% in 2026 feels less like a crisis and more like a reset. Investors repositioning older assets are quietly creating the next generation of office product.

Industrial

After years of overbuilding, supply and demand are finally aligning. A balanced industrial market is healthier for developers long-term. Absorption should rise, driven by logistics, e-commerce, manufacturing, and—importantly—data centers, which are absorbing industrial land in power-constrained markets.

Retail

The “retail apocalypse” headline is dead. Supply is tight, demand is stable, rents inch upward. Experience and value-based operators are outperforming.

Multifamily

Rent growth has slowed, but fundamentals are still intact. Developers have paused just enough to allow absorption to catch up. The opportunities in 2026 will be in operations: retention, cost control, right-sizing amenities, and managing through loan maturities that require recalibration.

Data Centers

The hottest asset class in the country, and arguably the one with the biggest mismatch between demand and deliverable supply. Power, land, and community resistance are the bottlenecks. Lease rates may rise again late in 2026.

Healthcare

The shift toward outpatient and neighborhood-level care continues. MOB occupancy above 92% speaks for itself. Aging demographics mean this sector will have long-term tailwinds independent of rate cycles.

Life Sciences

Still slow, still working through excess, but beginning to stabilize. If valuations improve and venture capital flows return, later 2026 could look very different.

Hospitality

Luxury and economy outperform for different reasons—wealth concentration and price sensitivity. Foreign tourism lags, but domestic demand remains strong.

Capital Markets

This is where optimism is returning:

Sales volume could rise 15–20%.

Pricing stability is back.

Investors are willing to step in again as risk becomes quantifiable.

Lenders are more inclined to extend than foreclose.

Cross-border capital is returning to U.S. CRE.

We’re not in a boom. We’re in a recalibration. And recalibrations reward disciplined operators.

4. The Connecting Thread: Real Estate Is Being Reshaped by Behavior, Not Headlines

If you zoom out, the three narratives—rental competitiveness, retirement migration, and macro resets—aren’t separate stories. They’re chapters of the same book.

Across every data point, one pattern jumps out:

Demand is reorganizing based on how people want to live, not based on the cycles economists expect.

Renters are staying longer. Retirees are diversifying their destinations. Companies are redefining their space needs. Consumers are prioritizing stability. Developers are tightening pipelines. And capital is once again gravitating toward quality and clarity.

This is why Miami, Chicago, and Manhattan can be simultaneously competitive.

It’s why Naples and Madison can both top retirement lists for very different reasons.

It’s why industrial and data centers are resetting while retail stays stable.

It’s why loan maturities may create opportunities instead of distress.

For those of us who build and invest in real estate, this moment is less about predicting cycles and more about understanding behavior. People vote with their feet long before the headlines catch up. They always have.

5. Looking Toward 2026: A Market That Rewards Discipline and Clarity

I expect 2026 to be a year defined by:

Tight but stabilizing rental markets as supply ebbs and flows.

Demographic-driven demand in both Sun Belt and non–Sun Belt metros.

An increasingly bifurcated CRE landscape where quality outperforms everything else.

Capital that becomes more selective but more active.

AI-driven productivity that benefits large operators first, then gradually trickles down.

A construction pipeline that stays constrained, which will push more value into existing assets.

In other words: the story is not risk or instability. The story is reorganization.

The operators who succeed in the next cycle won’t be the ones chasing trends. They’ll be the ones grounded in fundamentals, paying attention to demographic signals, and building where people genuinely want to live, work, and age.

That’s where I’m focused going into the new year.