THE KAUFMAN REPORT

· Kaufman & Company · thekaufmanco.com

Why the 85% permitting surge confirms what operators already knew — and what it means for the next cycle.

Market Analysis · May 2026

Let me be direct: we have been deliberately refocusing capital and attention back to our home market. Not because we’re sentimental about it — though I’ll admit I am — but because the data has been quietly building a case that most people weren’t paying attention to. The latest RealPage numbers just made it impossible to ignore.

Los Angeles multifamily permitting jumped 85% year over year to 15,735 units in the year ending March 2026. The city of Los Angeles alone — 11,378 units — sits at the top of every national ranking right now. That’s not a blip. That’s a structural reawakening.

What The Headlines Are Missing

Everyone will write about the 85% number. Very few people will contextualize what it actually means for those of us who build here.

For most of the post-pandemic cycle, Los Angeles got lapped. Austin was the darling. Phoenix was the growth story. Dallas was absorbing migration like a sponge. Meanwhile, LA was dealing with regulatory headwinds, expensive debt, land costs that never really corrected, and a political environment that made even the most patient developer reach for the antacids.

We stayed patient. We stayed in our market. We kept our eyes on the fundamentals that don’t move with headlines: supply constraint, renter demand density, transit connectivity, and the simple demographic reality that millions of people want to live here and there is nowhere near enough housing for them.

That’s Los Angeles. And the developers moving into Downtown, South Bay, Palms/Mar Vista, and Mid-Wilshire right now aren’t chasing a trend — they’re finally catching up to where the fundamentals have been pointing for years.

The Sun Belt Reckoning

I’ve been contrarian on several Sun Belt markets for a while now, particularly Florida. Not because those markets are bad — some of them are excellent — but because the narrative got so far ahead of the math that pricing stopped making sense for a disciplined operator.

The data is now catching up to that view. Orlando is pulling back. Austin — which was posting some of the most aggressive permit numbers in the country just two years ago — is among the sharpest national declines. Atlanta is softening. Rent growth is cooling in markets that got overbuilt during the pandemic apartment boom.

National Permitting Snapshot — Year Ending March

None of this surprises me. This is what happens when you add supply too fast into markets that were absorbing based on migration velocity rather than intrinsic demand depth. When migration slows — and it always does — you’re left with a lot of new product chasing fewer qualified renters.

Coastal gateway cities don’t have that problem. They have the opposite problem — chronically insufficient supply relative to demand. That’s not comfortable from an affordability standpoint, and I want to be clear that the housing shortage in Los Angeles is a genuine crisis for working families. But from a developer’s perspective, it is also the foundation of durable rent performance.

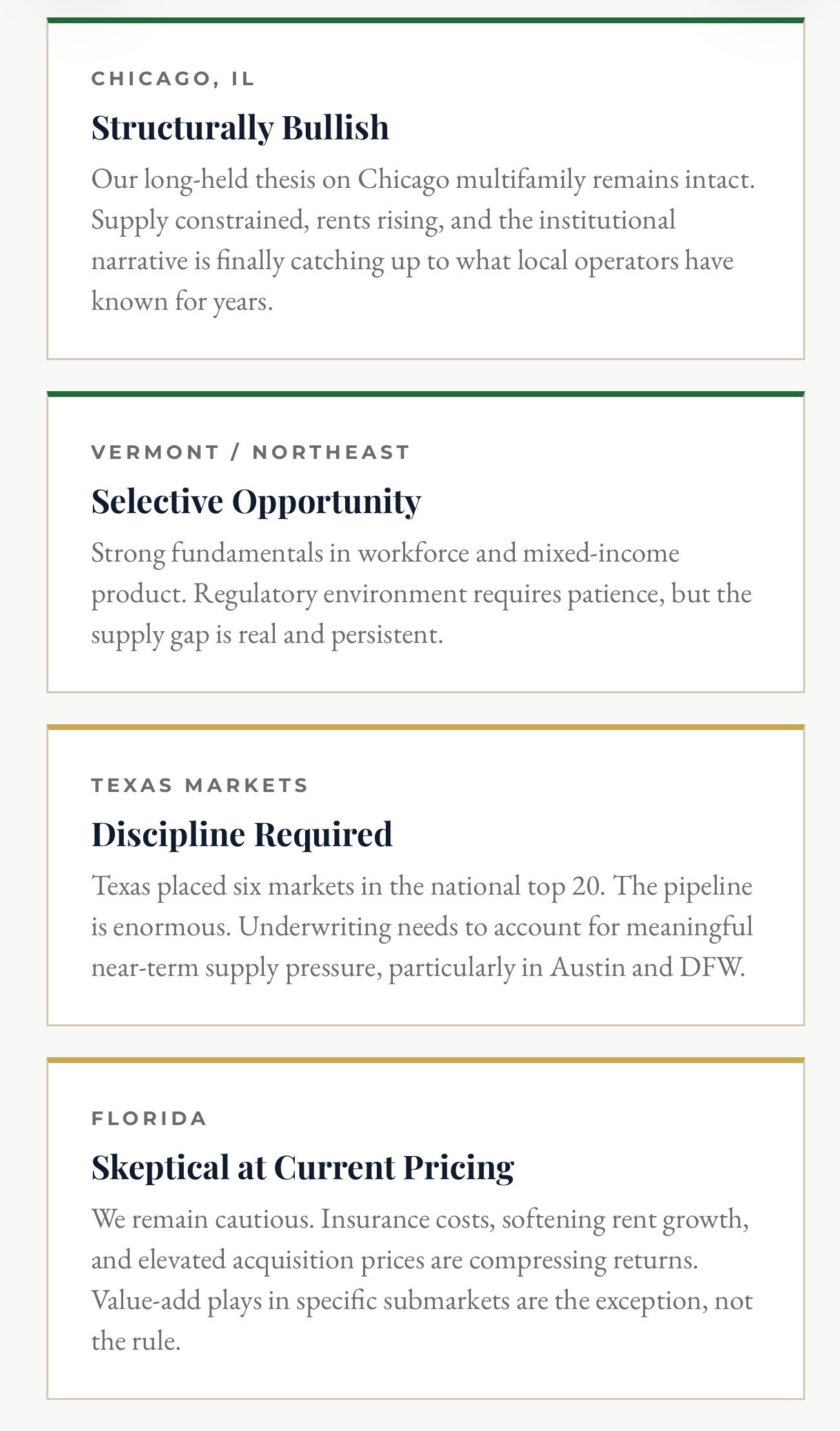

We remain cautious. Insurance costs, softening rent growth, and elevated acquisition prices are compressing returns. Value-add plays in specific submarkets are the exception, not the rule.

The Question Everyone Should Be Asking

Permits are leading indicators. They are not deliveries. The honest follow-up question is: how many of these 15,735 units actually break ground, and when?

Elevated interest rates are still a real constraint. Construction costs have not normalized — tariff-related materials exposure is a live issue that anyone actually building right now will tell you is not theoretical. Labor is tight. And Los Angeles entitlements, even when approved, don’t always convert quickly into shovels in the ground.

RealPage’s starts data is encouraging — activity is accelerating in several LA submarkets, which tells me the pipeline is not purely paper. But I want to see sustained starts data through Q3 and Q4 before I declare a full construction renaissance.

What I will say without hesitation is this: the direction is correct, and the fundamentals support it. Los Angeles is supply-constrained in a way that will not resolve itself quickly. Rents will continue to climb until deliveries catch up with demand. That gap is precisely where patient, disciplined operators have always found their returns.

Why We Are Bullish on Los Angeles — Full Stop

Let me be unambiguous about where we stand. We are bullish on Los Angeles real estate. Not cautiously optimistic. Not hedged with caveats. Bullish.

This city has 4 million people, a $1 trillion regional economy, world-class universities, the entertainment industry, a deepwater port, and a Mediterranean climate. The housing shortage here is not a policy accident — it is the result of decades of deliberate supply suppression through zoning, entitlement complexity, and NIMBY political pressure. That structural constraint does not reverse in one permitting cycle.

What does reverse is developer appetite and capital allocation — and both are clearly moving back toward Los Angeles. Infill urban development is getting done again. Submarkets that went quiet during the rate shock of 2023 and 2024 are showing real activity. The institutional money that fled to the Sun Belt is starting to remember why gateway cities exist at the top of every long-term allocation framework.

We have been here the whole time. We know these streets, these neighborhoods, these entitlement offices, these subcontractor relationships. Los Angeles is our home market for a reason — because over a long enough time horizon, supply-constrained, high-demand markets with genuine economic gravity always win.

The 85% permitting surge is a data point. The bigger story is that Los Angeles never stopped being one of the best long-term real estate markets in the world. The narrative just needed time to catch up with the reality.

It’s catching up now.

As always — originate with discipline, operate with intention, hold with conviction.