THE KAUFMAN REPORT

Real Estate · Capital Markets · Unfiltered

April 27, 2025

Private capital has quietly become the dominant force in commercial real estate. Here’s what that means for senior housing — and why it’s not a trend. It’s a structural shift.

Private Capital Reshapes the Playing Field

The 2026 Knight Frank Wealth Report confirmed what anyone operating in the market has already felt on the ground: private capital isn’t supplementing institutional real estate investment, it’s leading it. Family offices and high-net-worth investors are now setting prices and terms in major CRE transactions, including senior housing assets, across core global markets.

This isn’t a post-COVID anomaly. It’s the culmination of two decades of quiet accumulation. And senior housing is squarely in the crosshairs.

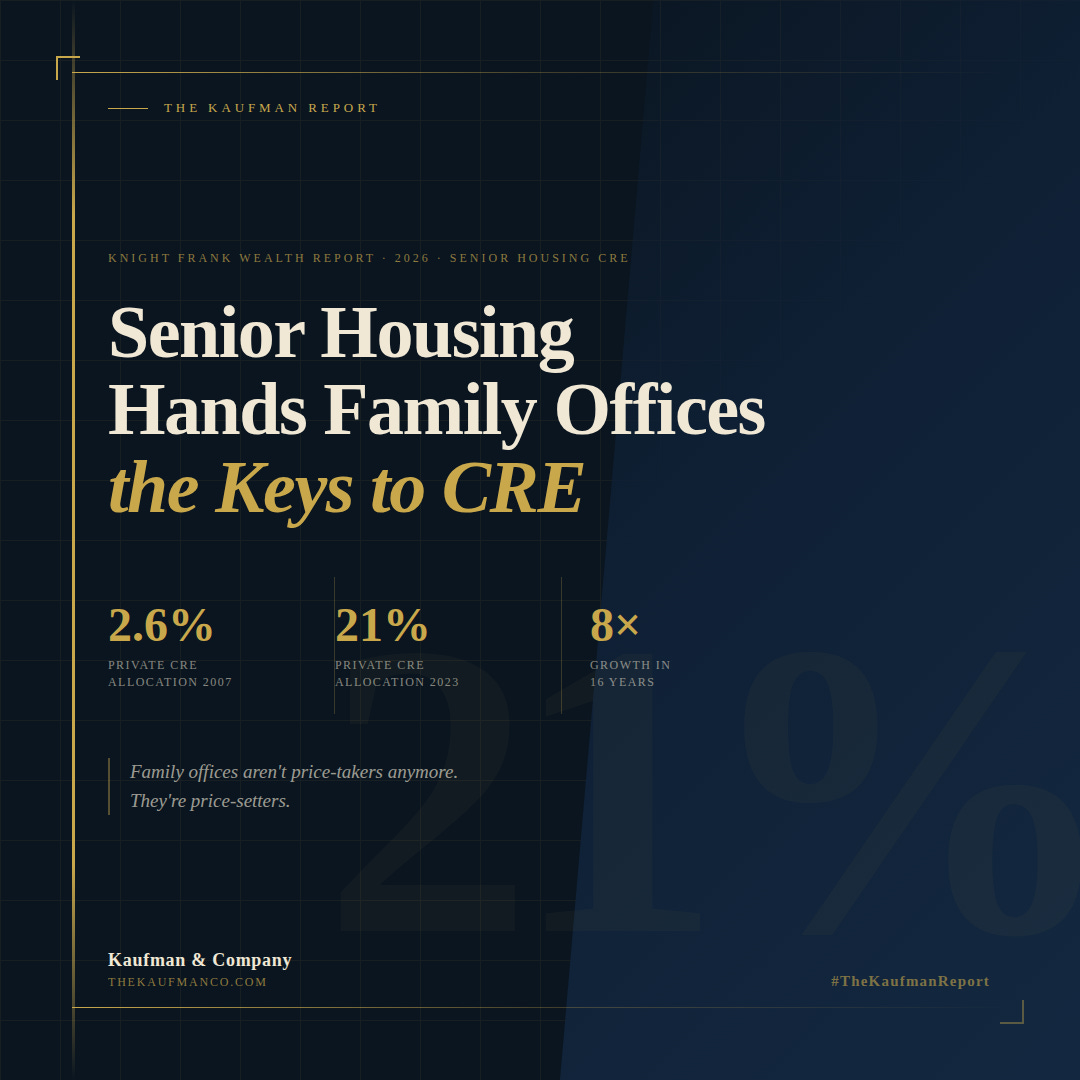

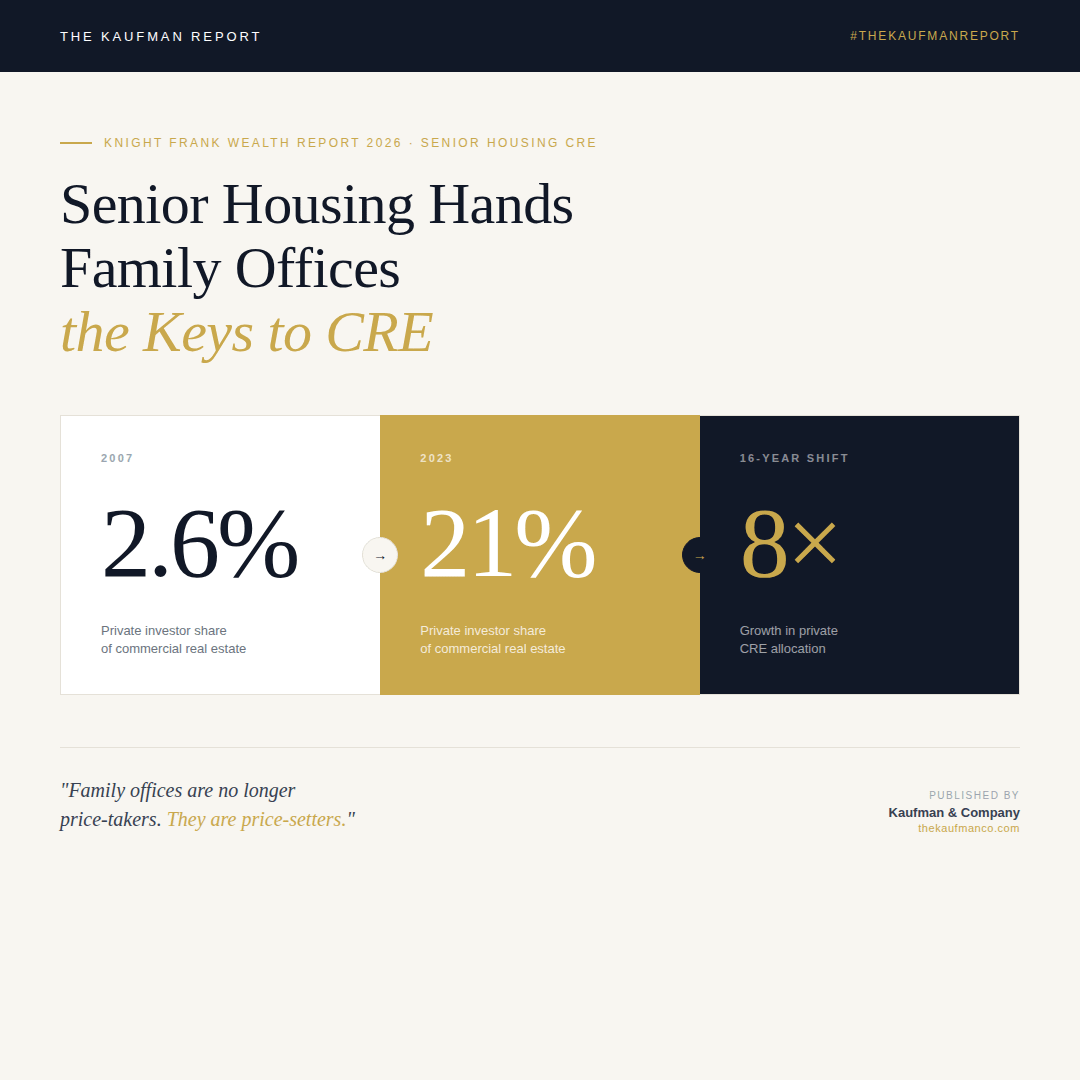

In 2007, private investors held just 2.6% of their wealth in commercial real estate. By 2023, that figure had climbed to 21%, an eightfold increase that reflects a deliberate, long-term rebalancing toward income-producing, inflation-resistant assets. Senior housing checks both boxes at a moment when it matters most.

Why Family Offices Are Accelerating — Not Slowing

The old knock on family offices was that they were undisciplined: trophy hunters chasing prestige assets with no real thesis. That era is over. Knight Frank’s data shows a dramatic professionalization of private investment offices over the past two decades. These are now sophisticated operations deploying dedicated real estate teams, underwriting with institutional rigor, and building portfolios designed to compound across generations, not quarters.

“Fewer reporting constraints, quicker decisions, flexible capital — family offices don’t just move faster than institutions. They move smarter when the window opens.”

The structural advantages are real and durable. Family offices aren’t subject to quarterly redemption pressures, committee approval chains, or the political calculus of public pension allocation. When institutional investors hesitate as they did during rate volatility, regional bank stress, and office sector contagion — private capital moves into the gap. Senior housing, with its demographic clarity and recurring revenue profile, has become a preferred destination for that capital.

Senior Housing: The Demographic Case Doesn’t Need a Bull Market

Most CRE sectors are cyclical bets. Senior housing is a demographic certainty. The aging of the Baby Boomer cohort creates sustained, multi-decade demand that doesn’t require a rate cut, a GDP print, or a Fed pivot to materialize. That’s the kind of demand profile that fits perfectly into a family office’s long-duration capital base patient money meeting a patient macro trend.

What the Knight Frank report makes clear is that family offices have already figured this out. They were providing liquidity in senior housing during periods of institutional retreat, and they are now positioned to continue shaping pricing and deal terms as the sector matures. For institutional players still sitting on the sidelines, the window to re-enter on favorable terms is narrowing.

What This Means for CRE Investors

The takeaway isn’t complicated, but it requires honesty: the competitive landscape in senior housing CRE has fundamentally changed. Family offices are no longer price-takers. They are price-setters. Any capital deployment strategy that treats private investors as secondary actors is operating with an outdated map.

Recalibrate accordingly. The firms that recognize private capital’s permanent, central role in senior housing — and structure their deal sourcing, partnerships, and financing accordingly, will be the ones with access when it matters. The rest will be reacting.

About Kaufman & Company

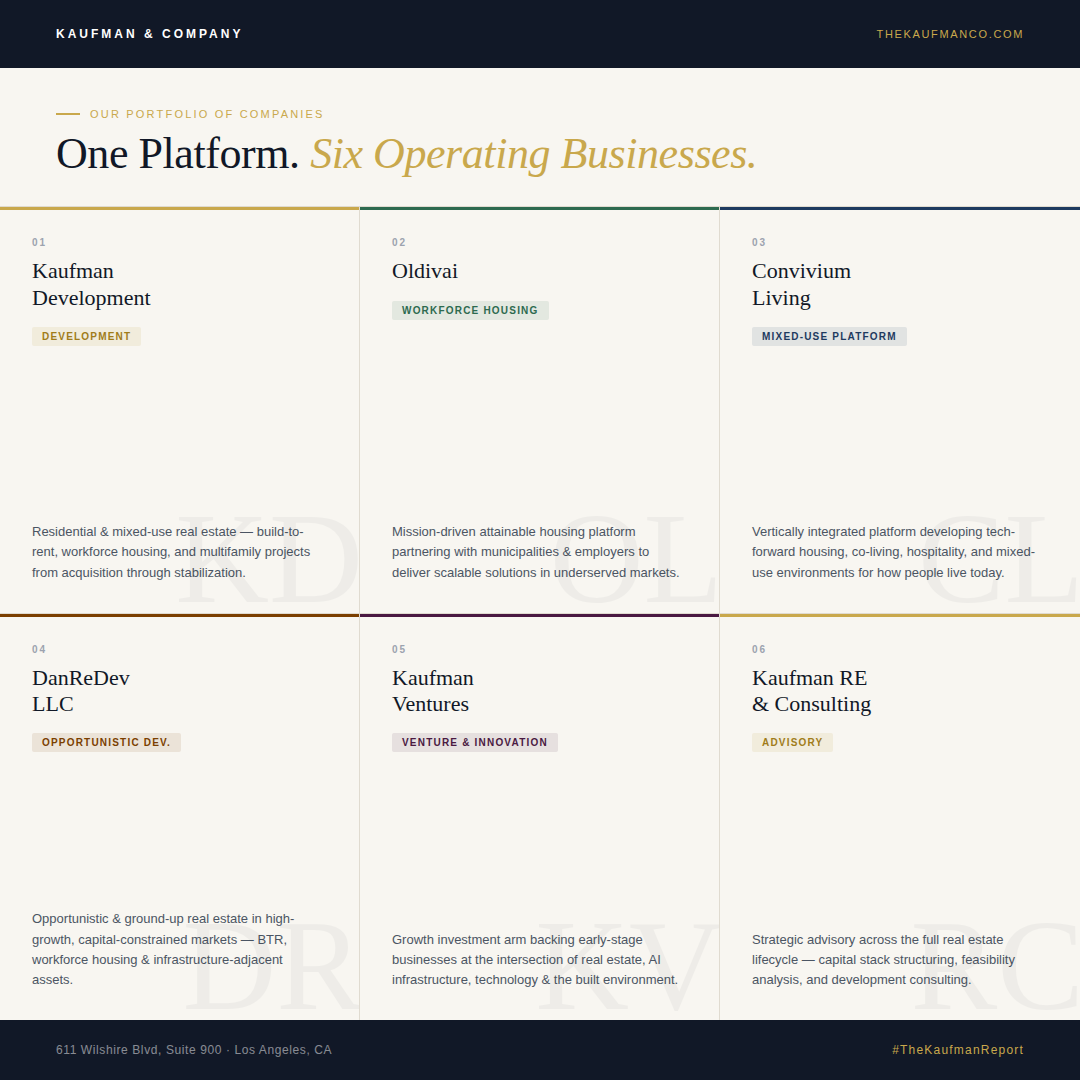

Kaufman & Company began as a family office. Over 25 years, it has evolved into something different, a full-spectrum real estate development and investment platform deploying capital across multifamily, workforce housing, resort development, and AI-driven infrastructure including micro data centers.

What hasn’t changed is the ethos: patient, conviction-based capital with an operator’s perspective. We don’t chase cycles. We underwrite demographics, structure for durability, and build for the long horizon. The shift private capital is making into senior housing CRE is one we understand from the inside because we’ve been making it ourselves.