Fueled by AI demand and a regulatory environment that, frankly, looks like a developer’s wish list, Texas is rapidly becoming the go-to destination for the next generation of massive, power-hungry data centers. If you just follow the capital, the cranes, and the interconnection queues, the story writes itself.

A Bloom Energy report projects that Texas will become the largest U.S. data center market within three years, driven almost entirely by AI workloads that demand unprecedented computing power. Energy use tied to data centers in the state is expected to rise from roughly 8 gigawatts in 2025 to over 40 gigawatts by 2028. That is not incremental growth. That is a structural rewrite of Texas’s power and land-use landscape.

The roster of players moving into the state reads like a who’s who of modern tech. Google, Nvidia, and Anthropic are ramping up projects across multiple Texas markets. Eric Schmidt and Rick Perry are backing large-scale efforts. Texas is also positioned to land part of “Project Stargate,” the $400 billion AI venture from OpenAI, Oracle, and SoftBank. In 2025 alone, Texas saw more than $3.4 billion in new data center construction, including $1.4 billion in December. These are not edge facilities or speculative shells. These are giga-scale, grid-bending projects.

The reasons Texas is winning new deals are not complicated. Cheap land. Relaxed regulations. Abundant natural gas. A political environment that does not reflexively try to slow-walk every major infrastructure project. As Bloom Energy’s Aman Joshi put it, “100 percent of onsite generation is largely happening with natural gas, and Texas certainly has a lot of access.”

Grid congestion and slow approvals elsewhere are pushing developers toward onsite power generation using natural gas and fuel cells. By 2030, one-third of U.S. data centers are expected to produce their own power. That is a fundamental shift in how real estate, utilities, and infrastructure finance intersect. By 2030, one in five U.S. data centers will exceed one gigawatt in demand. By 2035, that figure rises to one in three. This is not traditional industrial real estate. This is a new asset class with its own physics, its own capital stack, and its own political economy.

Texas is not just building data centers. It is rewriting the energy and development playbook.

But here is the part that gets lost in the breathless headlines.

Texas is growing fast, but it still trails Virginia, and Virginia is not just the U.S. leader, it is the data center capital of the world. And being number one comes with some very real negatives.

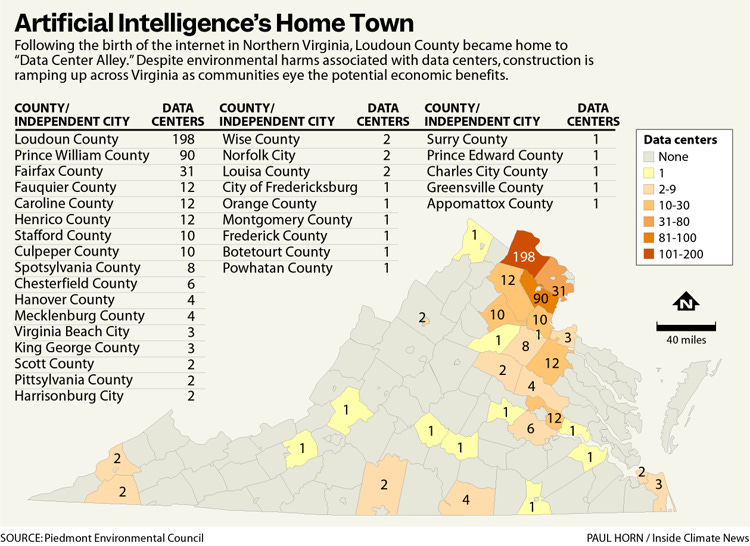

Drive up Route 28 in Loudoun County, Virginia, and you see it immediately. A dark blue box on the left. A gray one on the right. Transmission lines crisscrossing the sky to connect power to sprawling windowless buildings. These are not big-box retail stores. They are far bigger. They are data centers housing the physical backbone of the internet and artificial intelligence.

Northern Virginia dominates this industry for a simple set of historical and structural reasons. Proximity to Washington, D.C. and early federal research institutions like DARPA. The legacy footprint of America Online in the 1990s. Early investments in fiber. Cheap electricity. Available land near Dulles Airport. Aggressive state and local tax incentives. A utility willing to cut competitive power deals. The flywheel took off, and it never stopped.

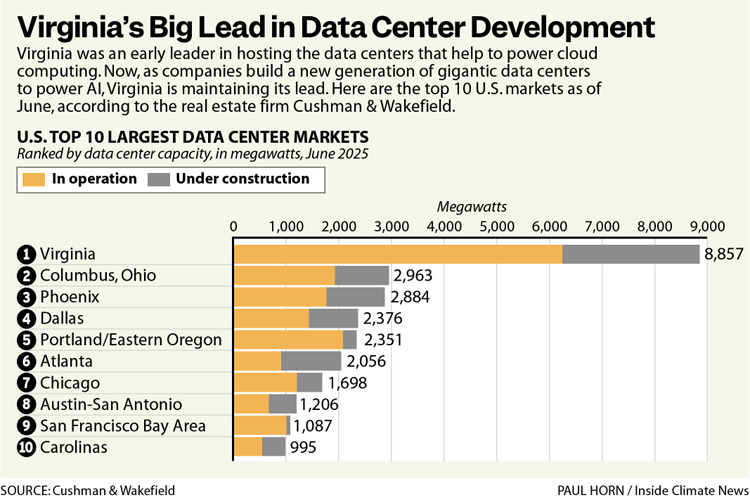

As of June, Virginia had 6,247 megawatts of data centers operating and another 2,610 megawatts under construction. That combined 8,857 megawatts is nearly triple the operating and under-construction capacity of the next market, Columbus, Ohio. The most striking figure is planned capacity, 24,103 megawatts.

No market in the world comes anywhere close.

And here is the uncomfortable part.

Behind those massive numbers is a very small one. Data centers do not employ many people. Virginia’s data center operations supported just 12,140 operational jobs in 2023. That is slightly fewer than the number of school bus drivers in the state. Even if you zoom out to include construction and indirect jobs, you are still talking about 78,140 roles tied to an industry that is consuming land, water, and electricity at a staggering pace.

Environmental advocates have a point when they argue that the local costs may exceed the benefits. Vanishing farmland. Rising water consumption for cooling. Grid strain. Carbon emissions. Electricity demand growing faster than utilities can reasonably plan for. Dominion Energy is projecting demand rising from 17,300 megawatts last year to 26,600 megawatts by 2039, with data centers as the primary driver. The utility is now asking regulators to approve rate increases that could raise the typical household bill by roughly $21 per month by 2027.

That is the hidden tax of being number one.

There is also the political blowback. Loudoun County now treats data center development as a campaign issue. Public resistance is rising. Regulatory scrutiny is increasing. Conservation groups are increasingly vocal. A proposed 2.2 million square foot facility in rural Remington, Virginia would have needed 800 megawatts, nearly the peak load of the entire state of Vermont. The developers withdrew and are now pitching a smaller version.

This is what scale looks like when it collides with real communities.

Virginia’s transformation into the data center capital of the world is, on paper, a business success story. Loudoun County officials point to $1 billion in annual tax revenue from data centers, funding roughly one-third of the county’s budget. Residential tax rates have been cut materially. Schools and public services have benefited.

But the question that is now mainstream in Virginia, and will eventually become mainstream in Texas, is whether the tradeoffs are worth it.

These buildings are essentially self-operating. They fill the landscape. They reshape energy planning. They drive massive capital flows. But they do not create vibrant employment ecosystems the way traditional commercial or industrial development does.

As a developer and investor who is deeply involved in AI-driven real estate and data center infrastructure, I see both sides of this clearly.

Texas is absolutely the next major growth engine for data centers. It has the land. It has the gas. It has the political will. It has the capital. It is going to capture a massive share of next-generation AI infrastructure.

But Virginia’s experience is a cautionary tale.

Being the global capital of anything at giga-scale comes with unintended consequences. Grid strain. Environmental pushback. Community resistance. Ratepayer pain. And very real questions about long-term economic efficiency if AI capital deployment outpaces actual monetization.

There is also concentration risk. When Amazon Web Services outages ripple across the internet because too much infrastructure is clustered in Northern Virginia, that is not just a technical problem. That is a systemic vulnerability.

We urgently need geographic diversification in cloud and AI infrastructure. Not just for resiliency, but for political sustainability.

Texas is in the early innings of a Virginia-scale transformation. It will almost certainly overtake Virginia in raw capacity growth over time. But if Texas wants to avoid inheriting Virginia’s political, environmental, and grid headaches, it will have to do something Virginia never really did.

Plan holistically.

That means aligning land use, grid expansion, onsite generation, water resources, community engagement, and ratepayer protection from day one. It means not just chasing cheap land and fast permits. It means acknowledging that giga-scale data centers are not just real estate projects. They are public infrastructure projects in private clothing.

The AI era is still in its early stages. The real estate and energy decisions being made right now in Texas will shape the next thirty years of American digital infrastructure.

Virginia already ran that experiment.

Texas still has the chance to run it better.