The metros winning the AI workforce race aren’t just tech stories. They’re real estate stories.

Everyone wants to talk about AI as a technology trend. I want to talk about it as a geography problem — because that’s what it is from where I sit.

AI job growth in the United States is not distributed. It’s concentrated. And highly concentrated labor markets have a way of reshaping real estate fundamentals faster than most developers and investors are prepared for.

Let me break down what the data is actually telling us.

The Usual Suspects Are Still Winning — But the Map Is Getting More Interesting

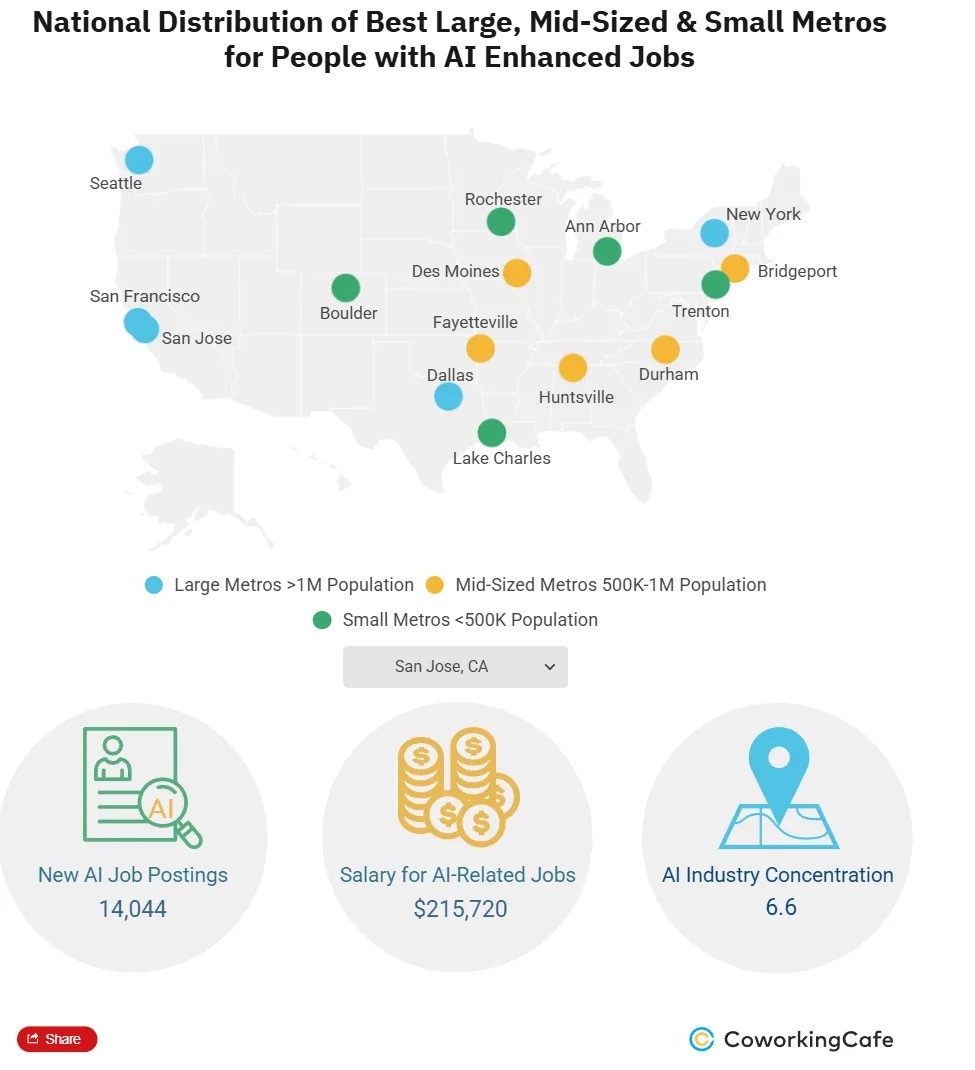

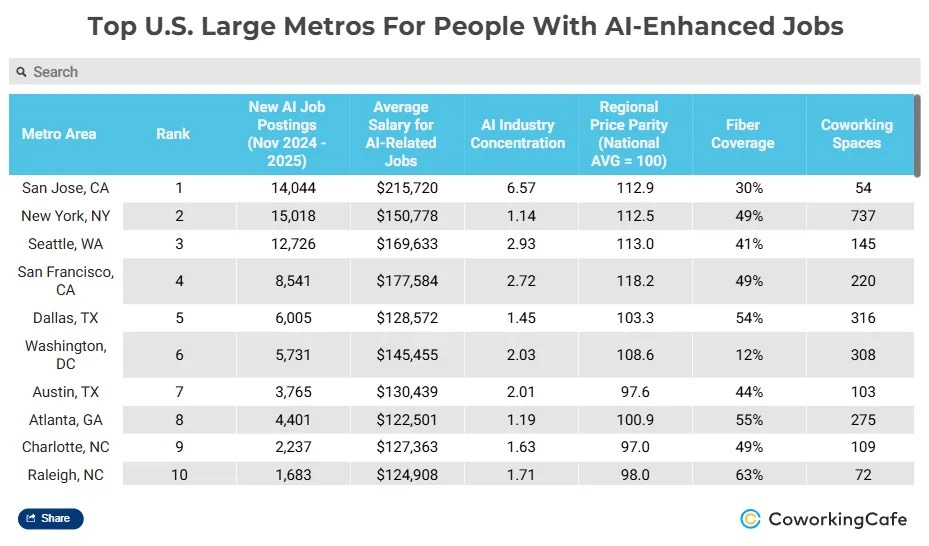

San Jose remains the undisputed center of gravity for AI talent. The metro’s concentration of AI jobs runs more than six times the national average, and average salaries are pushing $215,000. That’s not a labor market. That’s a pressure cooker.

New York has quietly become the volume leader — over 15,000 new AI job listings, more than any other metro in the country. Salaries average around $151,000, well below Silicon Valley, but New York has something San Jose doesn’t: scale, diversification, and a talent pipeline that draws from finance, media, academia, and tech simultaneously. The city isn’t trying to be Silicon Valley. It doesn’t need to be.

Seattle and San Francisco remain essential nodes in the AI ecosystem, both for pay and specialization. But high costs continue to compress real returns for workers and strain developers trying to underwrite workforce and market-rate housing anywhere near these cores.

This is not new information. What is worth paying attention to is what’s happening in the second tier.

Dallas Is Making a Serious Move

I’ve been bullish on Dallas for a while, and the AI workforce data reinforces why.

The market combines $128,000 average AI salaries with strong fiber infrastructure, 316 coworking spaces, and a cost-of-living profile that doesn’t punish workers for showing up. That spread — solid compensation without the coastal tax — is exactly what drives sustained in-migration and, by extension, sustained housing demand.

For developers underwriting multifamily or build-to-rent in the Dallas metro, this isn’t a minor tailwind. A knowledge-economy workforce growing in place, with rising incomes and below-average housing costs relative to competing markets, is about as clean a demand driver as you’ll find in today’s environment.

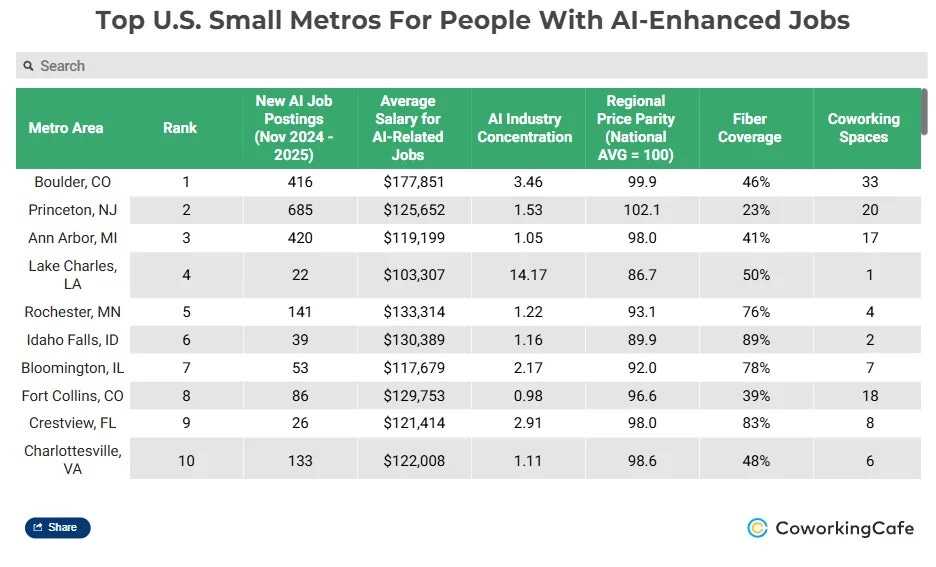

The Small Metro Signal Is Real, and Most People Are Missing It

Boulder, Colorado is posting the highest AI specialization and pay among small metros at $177,851 average. Princeton, Ann Arbor, Fayetteville, Huntsville — these aren’t flukes. These are markets where research institutions, lower operating costs, and remote-work flexibility are combining to create genuine AI workforce density in places that couldn’t have competed for this talent five years ago.

I’ve been paying close attention to secondary and tertiary market dynamics across our platforms — both through Oldivai and through our broader development pipeline — and what I keep seeing is that the workforce follows the work. When AI companies and adjacent employers set up distributed teams or remote hubs in mid-sized metros, they create self-reinforcing demand cycles for housing, coworking, and mixed-use amenities.

Fayetteville and Huntsville are early examples of a pattern I expect to see repeat across more markets over the next decade. Don’t underestimate them because they’re not on the standard institutional shortlist.

Infrastructure Is the Underlying Bet

Here’s the part that gets buried in most coverage of this data but shouldn’t: fiber coverage and coworking density are emerging as material site-selection criteria for AI employers — and by extension, for the workers they’re recruiting.

This matters directly to how we underwrite assets in markets where AI-driven growth is accelerating. A market with strong digital infrastructure, accessible coworking, and a workforce that can function effectively in hybrid or distributed environments has a meaningfully different demand profile than a market without those attributes. The gap is widening, not narrowing.

At Kaufman Development and through our DanReDev platform, we think about infrastructure as a real estate input — not just a background condition. Where fiber coverage is strong, where hybrid work infrastructure is mature, and where cost structures don’t force workers to choose between career opportunity and quality of life, you get the conditions for durable, compounding demand.

What I’m Watching

The AI talent geography story is still early. The current concentration in San Jose, New York, and Seattle will not hold indefinitely. Cost pressures, hybrid work normalization, and deliberate employer diversification will continue pushing AI jobs into new markets. Dallas is the obvious next major hub. Boulder, Durham, and Huntsville represent the emerging edge.

For developers and investors, the question isn’t which city wins the AI race. It’s which markets are building the housing, infrastructure, and urban fabric that knowledge workers will actually want to live in — and which ones are going to wake up in five years wondering where the demand went.

That’s the analysis I’m tracking. It shows up in every underwriting conversation I’m having right now.

Daniel Kaufman is the Founder and CEO of Kaufman & Company, a Los Angeles-based real estate development and investment platform. Follow The Kaufman Report on Substack for ongoing market analysis, deal intelligence, and development strategy.