The fastest-growing cities in America aren’t cities at all. They’re the places people fled to when cities stopped working.

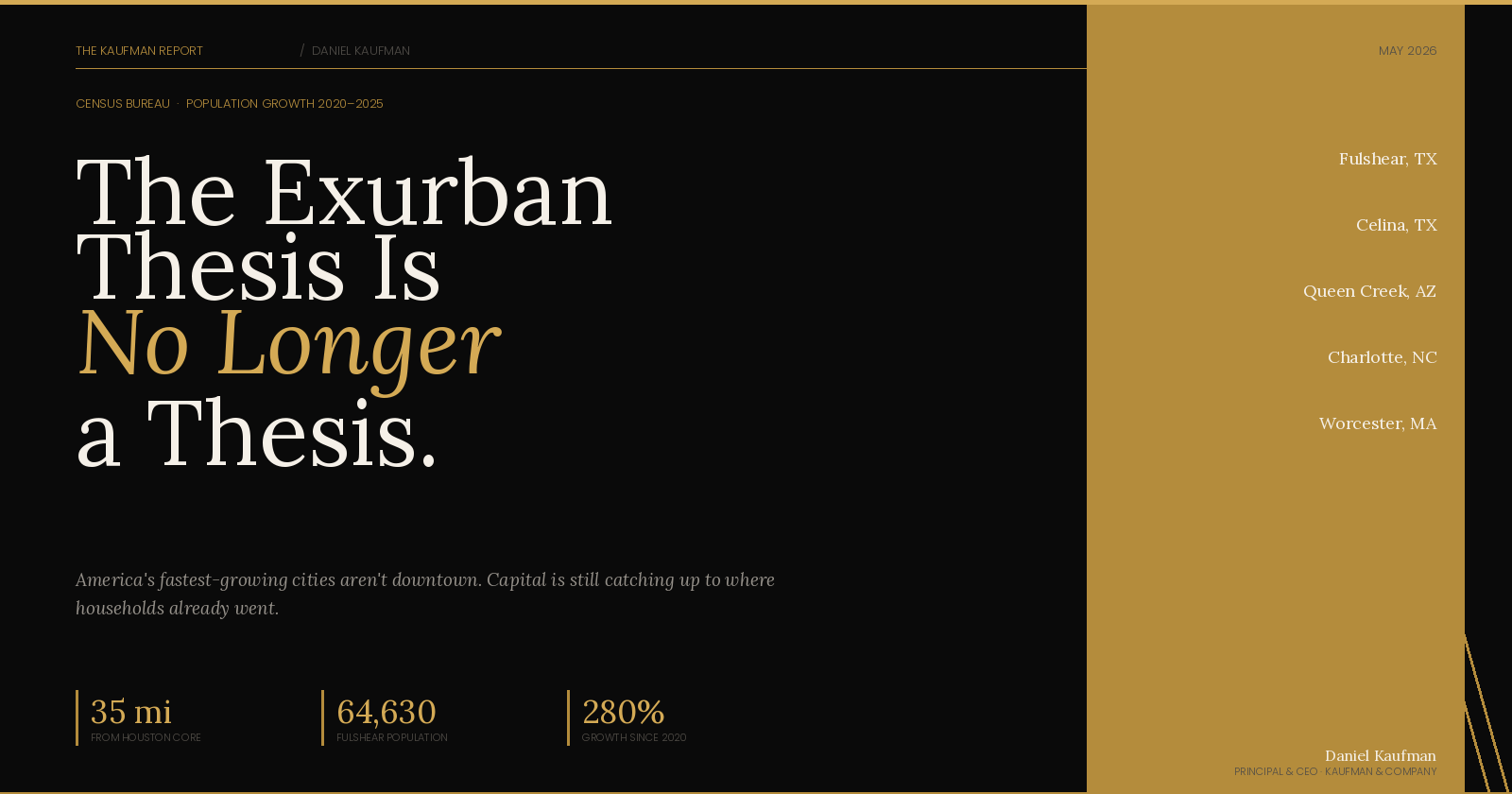

Fulshear, Texas. Population: 64,630. Growth since 2020: nearly 280%. Distance from downtown Houston: 35 miles. The Census Bureau just confirmed what developers who were paying attention already knew — the American growth map has been redrawn, and it wasn’t drawn by urban planners.

This isn’t a Sun Belt story. It’s not a remote work story. It’s a math story.

What the Census Data Actually Says

The new numbers are worth sitting with. Fulshear — a master-planned exurb most people couldn’t place on a map — was the fastest-growing U.S. city with more than 50,000 residents between 2020 and mid-2025. Celina, north of Dallas, added nearly 13,000 residents in a single year. Queen Creek, outside Phoenix, expanded 8.2% and is closing in on 90,000 residents. Charlotte is nearing one million people — growing faster last year than any other U.S. city with over 500,000.

Meanwhile, Dallas posted a slight population decline. Houston — a city of 2.4 million — added fewer new residents than some of its own exurban satellites.

That inversion is important. The core isn’t the growth engine anymore. The periphery is.

Why This Matters More Than the Headlines Suggest

Every cycle, the narrative resets. In the 2010s, it was urban densification — everyone moving back downtown, transit-oriented development, the death of the suburbs. Developers who believed that narrative and paid urban infill premiums got a painful education in how wrong consensus thinking can be.

The exurban thesis runs on simpler inputs: land cost, home size, school quality, and commute tolerance. When those variables shift — and they have shifted permanently — capital follows households, not the other way around.

What’s moving to Celina and Fulshear and Goodyear isn’t a demographic anomaly. It’s a rational household decision at scale. Larger home. Newer community. Functional infrastructure. Price points that don’t require a dual-income household earning $250,000 to qualify.

The demand is real. The question is whether the supply side catches up — and right now, it’s not.

The New England Angle (Which Nobody Is Talking About)

Boston’s affordability ceiling is well-documented. What’s less discussed is where that pressure is actually landing.

Worcester is at nearly 214,000 residents. Manchester and Nashua keep absorbing Boston-market refugees priced out of the metro. Everett — three miles from Boston — posted 4.6% population growth amid a recent housing development cycle. These aren’t secondary markets anymore. They’re the primary growth markets in the region, operating under the radar of capital that’s still fighting over Seaport parcels.

The pattern mirrors what Texas figured out a decade ago: when a core city prices out its own workforce, the workforce leaves — and it takes its household formation with it.

What This Means for Capital Allocation

National population growth slowed to 0.5% last year, roughly half the prior pace. Immigration restriction is a real headwind on the demand side. The macro is not as favorable as it was in 2021.

But the spatial distribution of that demand has shifted in ways that are durable, not cyclical.

The developers who are positioned in exurban Texas, outer-ring Arizona, and secondary New England markets aren’t riding a trend. They’re riding a structural reconfiguration of where Americans want to live — and more importantly, where they can afford to live.

Infrastructure follows rooftops. Retail follows rooftops. Multifamily follows rooftops. Industrial follows distribution needs generated by population. The entire real estate investment thesis downstream of household location decisions runs through this data.

The Operator’s Read

I’ve spent 25 years watching capital chase consensus narratives into overpriced markets and miss the structural shifts that were visible in the data the whole time.

The exurban growth story isn’t new. What’s new is the scale and the permanence. Fulshear at 64,000 residents is a city now. Celina is a city now. These aren’t bedroom communities — they’re economic units that generate their own demand for multifamily, retail, and services.

The next wave of development opportunity in this country isn’t in urban infill. It’s in the land that was cheap enough to actually build on — and is now filling up faster than anyone projected.

Follow the households. The capital always gets there eventually.

Daniel Kaufman is the Principal & CEO of Kaufman & Company, a vertically integrated real estate development, investment, and private lending platform based in Los Angeles. He has developed more than 10,000 multifamily units across the U.S. without outside capital.