April 2026 · Florida Market Intelligence

Forget the brokers on Instagram and the media cheerleaders. The numbers on the ground tell a different story — and operators need to hear it straight.

I’ve been skeptical of Florida as a real estate thesis for a while now. Not because I don’t understand the appeal — the tax structure, the weather, the narrative. I get it. But narratives don’t service debt. Fundamentals do. And the fundamentals in Florida have been deteriorating in ways that most people selling you deals down there don’t want to talk about.

The Wall Street Journal just ran a piece on Florida’s population boom fizzling as high costs drive away the middle class. It’s a good article. But the data goes deeper than one news cycle. Let me give you what the brokers aren’t posting.

The Migration Story Is Over — and the Numbers Are Brutal

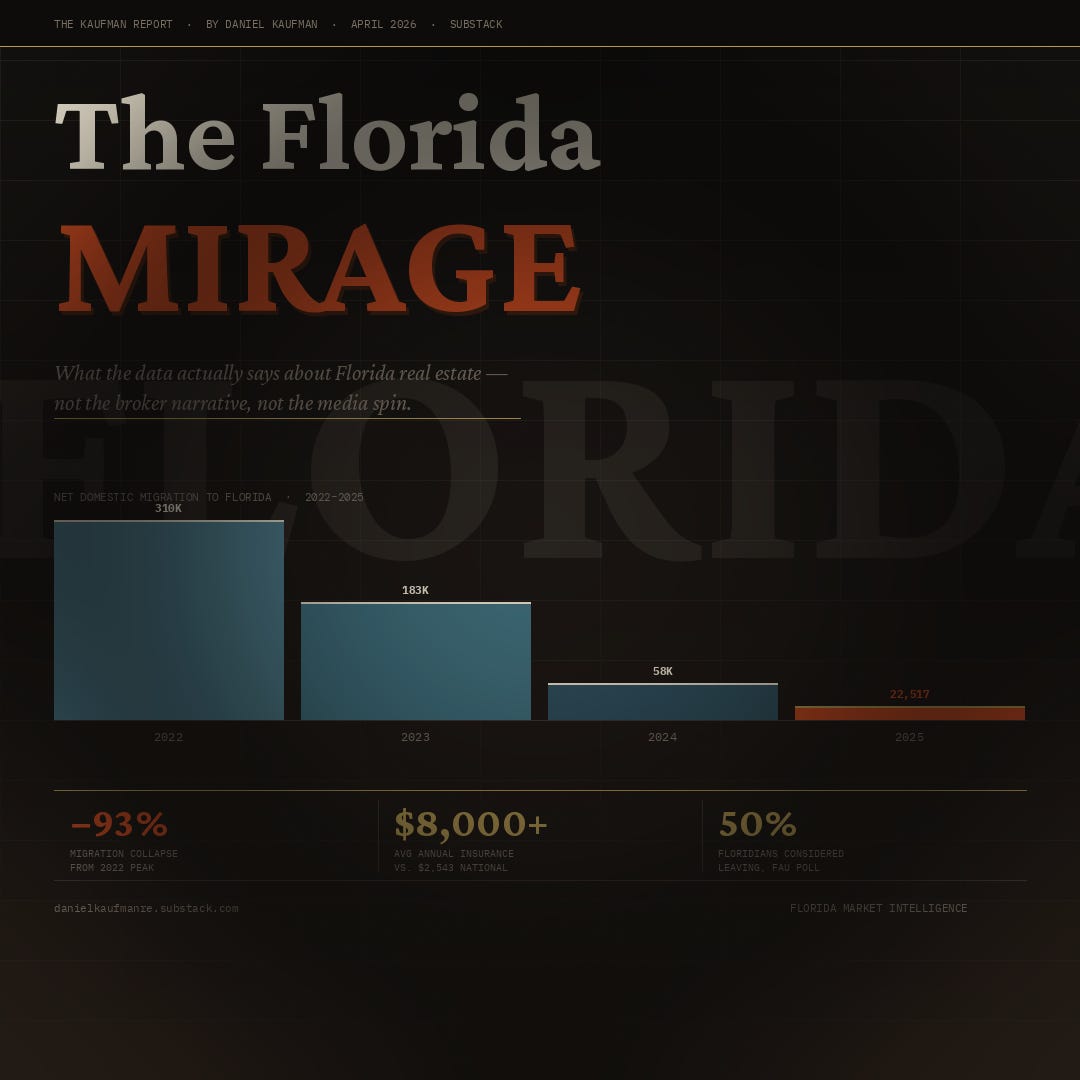

The single most important fact about Florida right now is this: net domestic migration to Florida fell from 310,892 in 2022 to just 22,517 in 2025 — a 93% collapse from peak in three years.

Let that land. Ninety-three percent.

Florida has fallen from the nation’s top destination for domestic movers to the number eight spot, now trailing South Carolina, Idaho, North Carolina, Texas, and Utah, among others.

The pandemic migration trade is done. The people who were going to move to Florida for tax advantages and sunshine and remote work flexibility already moved. The ones who came during the boom are now discovering what it actually costs to live there. And a meaningful portion of them are leaving.

A poll by Florida Atlantic University’s Business and Economics Polling Initiative found that 80% of Florida residents were concerned about housing affordability, and 43% said they lived paycheck to paycheck. Nearly half said they had considered leaving Florida because of the cost of living.

Nearly half. In a state that was supposed to be the promised land of affordability.

Who’s Leaving and Who’s Arriving — The Demographic Swap

Here’s the part that should concern anyone underwriting long-term Florida growth: the people leaving aren’t the retirees. While Florida saw an influx of residents aged 60 and older, younger residents — particularly those aged 20 to 29 — are leaving in significant numbers. Factors cited include the high cost of housing and limited in-state job opportunities for early-career professionals.

Younger residents are leaving the state, likely due to cost considerations, and being replaced by older arrivals less attached to the labor force. That demographic shift may already be contributing to a slowdown in the growth of the labor force.

Think about what that means for a real estate market. You’re trading working-age renters and buyers for retirees on fixed incomes. You’re bleeding the workforce that fills your apartments and buys your starter homes, and replacing it with people who aren’t going to drive the kind of economic activity that justifies the valuations built into a lot of Florida deals right now.

Of the 20 most common occupations in the state, 13 paid on average less than $20 an hour, including retail salespeople, cashiers, and cooks, according to a 2025 study by United Way of Florida.  This is not a market where the workforce is keeping pace with the cost of the real estate it’s supposed to occupy.

The Insurance Crisis Isn’t a Headline — It’s a Structural Reset

The insurance story in Florida is not a temporary dislocation. It is a permanent repricing of climate and litigation risk that has fundamentally changed the carrying cost math for anyone owning real estate in the state.

Florida homeowners pay 4.5 times the national average for property insurance — approximately $8,000 or more annually — which alone reduces a buyer’s purchasing power by roughly $100,000 compared to states with average insurance rates.

Read that again: $100,000 in lost purchasing power. Before you look at the price of the house.

Many insurance carriers have withdrawn from the state’s condo market entirely as climate risks spike, driving up HOA dues and forcing associations to either raise monthly fees, accept policies with reduced coverage, or both — creating a vicious cycle that further depresses condo values and marketability.

The condo market specifically is in a category of its own kind of trouble.

The Condo Crisis: Surfside’s Long Shadow

The 2021 Surfside collapse didn’t just kill 98 people. It killed the business model for a significant portion of Florida’s coastal condo inventory. The legislation that followed — mandating structural inspections and fully funded reserves for older buildings — set off a chain reaction that the market is still absorbing.

Special assessments ranging from $20,000 to $400,000 per unit have made many buildings effectively unmarketable. When an association’s insurance lapses or reserves are materially underfunded, the building loses its “warrantable” status — cutting off conventional financing for all units in the building, limiting the buyer pool to cash purchasers or those with access to portfolio loans at higher rates.

40% of condo owners faced special assessments in the last three years.  That is not a niche problem. That is a systemic one.

Miami-Dade condo inventory reached 13.2 months’ supply, while Broward County hit 9.84 months’ supply — both well above the six-month threshold that defines a balanced market.

A 13-month supply of condos in Miami-Dade. That number should be in every underwriting memo for anyone looking at Florida multifamily or condo product right now.

The Price Data: What the Medians Hide

The headline number brokers like to cite — Florida’s statewide median home price — obscures more than it reveals. Here’s what the disaggregated data shows:

The FHFA index is down 2.3% year-over-year as of Q3 2025. Case-Shiller shows Tampa down 3.9% and Miami down 1.0%. Price cuts are widespread — 33.6% of active listings have price reductions, and in Southwest Florida metros, that figure exceeds 40%.

Florida’s median home value dropped approximately 5% over the past year, from around $396,000 to about $374,000 as of November 2025. As of late 2025, homes across the state spent a median of 80 days on the market — well above the national median of 50 days.

The base case forecast calls for statewide prices to decline an additional 2 to 4% through year-end 2026, with Southwest Florida condos experiencing 8 to 15% peak-to-trough declines. This is not a bubble pop — it is a structural repricing of carrying costs that the market is still absorbing.

And the supply side isn’t helping. January 2026 set a record for new listings in Florida — the most for any January going back to 2008, with single-family new listings up 7% year-over-year and condo listings up 2.7%.

More supply, less demand, higher carrying costs. That is not a setup that resolves quickly.

The Foreclosure Signal

Florida leads the nation in foreclosure activity, with 0.44% of homes receiving filings in 2025 and 4,962 filings in January 2026 alone.

The distress is arriving. It’s early innings. But it is real, it is measurable, and it will intensify as the insurance squeeze forces more owners — particularly in the condo market — to list or default regardless of what their mortgage rate is. The rate-lock effect that has suppressed inventory nationally is weaker in Florida precisely because the HOA and insurance cost burden is forcing involuntary sales.

The One Honest Broker Take

To be fair about the complexity here: Florida is not one market. Miami luxury, backed by Latin American and international cash buyers, operates on a different set of inputs than Cape Coral or the condos along the Gulf Coast. The demand for Miami real estate from domestic and international buyers remains steady, and Miami-Dade continues to attract buyers from Latin America who seek a cultural city, buyers from California and New York who seek tax benefits, and companies relocating their headquarters or regional offices to South Florida.

Florida remains one of the country’s top relocation destinations — fourth nationally for net migration interest, behind North Carolina, South Carolina, and Tennessee.  The state isn’t dying. The narrative of inevitable, frictionless growth is.

What This Means for Operators

Here’s my read — unhedged, as an operator who has been watching this market and consciously staying out of most of it:

The Florida trade worked when you had three tailwinds stacking simultaneously: population inflow, low interest rates, and insurance costs that were expensive but manageable. All three of those tailwinds are now either headwinds or significantly diminished. What’s left is a market that still has long-term demand but is working through a painful repricing of carrying costs that has years, not quarters, to run.

The opportunities that will emerge in Florida will be distressed ones — forced sales from condo owners hit with six-figure special assessments, insurance-driven defaults in coastal markets, developers who over-leveraged during the boom holding unsold inventory. That’s a workout play, not a growth play. And it requires a completely different underwriting model than what got deployed into this market between 2020 and 2023.

The brokers posting sunset photos and cap rate projections on Instagram are not lying to you. They’re just not telling you about the $8,000 insurance bill, the $134,000 special assessment, the 80 days on market, or the 93% collapse in the net migration that was supposed to justify all of it.

The data is publicly available. Read it before you wire a deposit.

Daniel Kaufman is the Principal & CEO of Kaufman & Company, a vertically integrated real estate development and investment firm. The Kaufman & Company Report publishes independent market analysis from an operator’s perspective.

RealDanielKaufman.com · @realdanielkaufman