The numbers are in, and they don’t lie — though plenty of people will try to spin them.

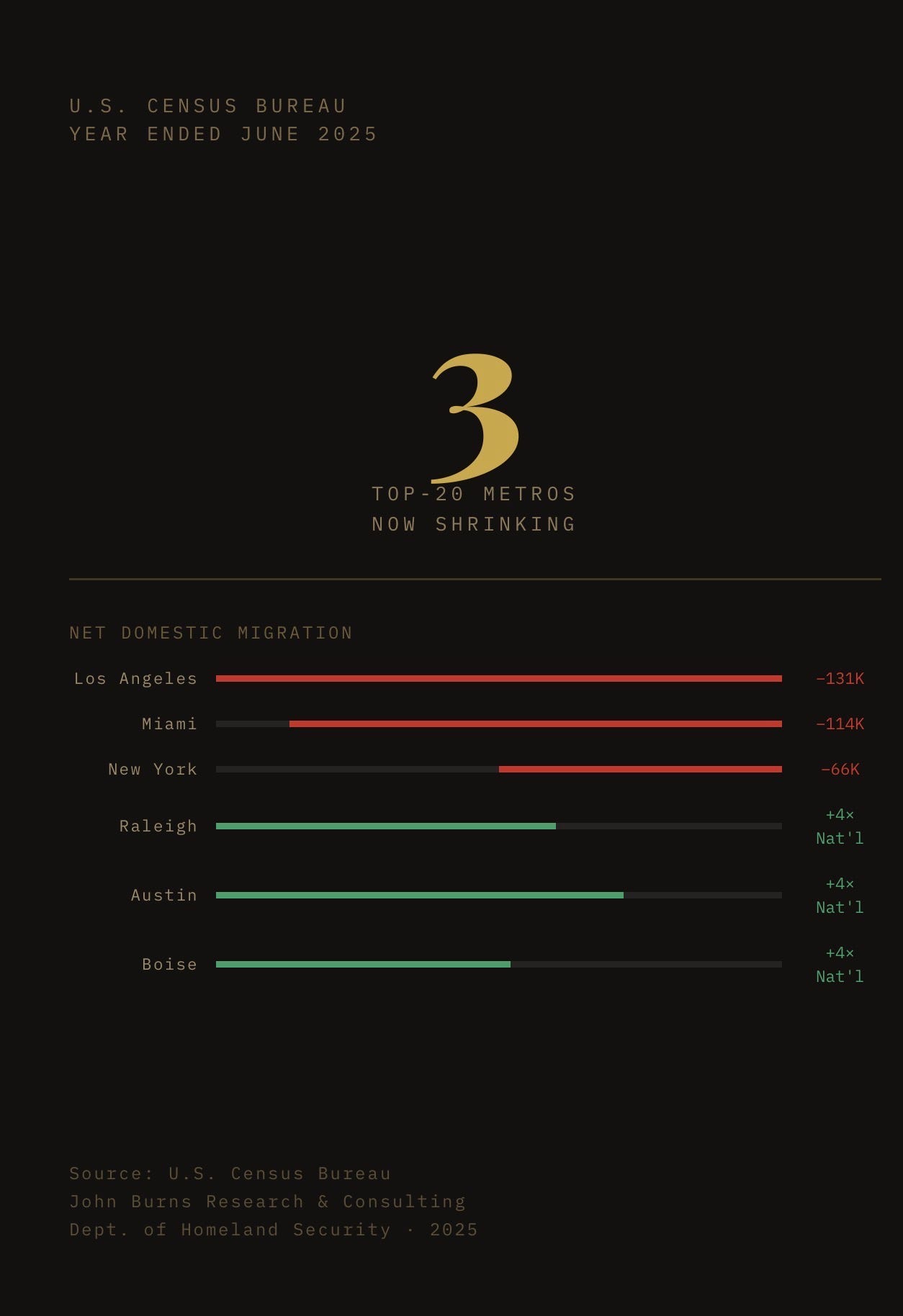

The Census Bureau just dropped metro-level population estimates through June 2025, and the headline is jarring for anyone with capital deployed in America’s biggest urban markets: Los Angeles, San Diego, and Miami — three of the 20 largest metros in the country — are shrinking. New York City slipped back into negative territory for the first time in three years.

Let that sink in for a moment.

What’s Actually Happening

This isn’t a mystery. It’s arithmetic.

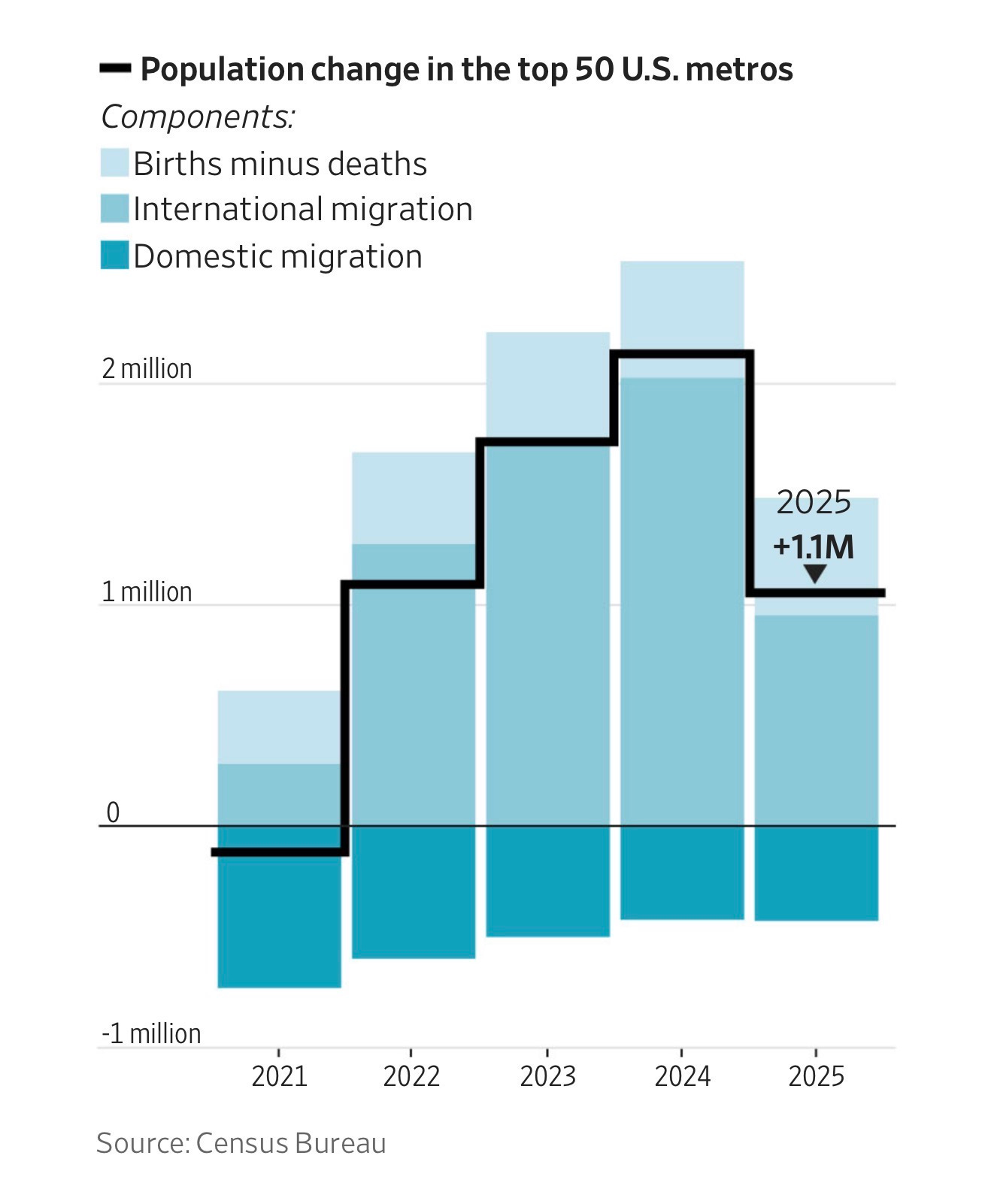

Population growth has three levers: domestic migration (people moving between states), international migration (immigrants arriving net of those leaving), and natural increase (births minus deaths). In the big coastal metros, all three are moving in the wrong direction simultaneously.

The immigration spigot — which had been running hard enough to paper over the domestic outflow — has essentially been turned off. The U.S. saw 675,000 deportations in Trump’s first year back in office. A recent WSJ analysis suggests that for the first time since the Great Depression, more people may have left the U.S. than arrived last year.

In Los Angeles, net immigration added about 38,500 people. Domestic outmigration subtracted nearly 131,000. You don’t need a PhD in demography to see how that math ends.

Miami tells the same story. The region lost nearly 114,000 residents on a net domestic basis — people voting with their U-Hauls for cheaper, less congested markets. The immigration buffer that was softening that blow has largely evaporated.

This is what policy-driven demographic change looks like in real time. As John Burns Research puts it plainly: “The vast majority of the slowdown of immigration is because of policy shifts.” This isn’t cyclical. This is structural, and it’s going to persist for as long as current enforcement posture holds.

What It Means for Real Estate

I’ve been watching the capital flows closely, and here’s what I’m seeing on the ground.

The big coastal metros are in structural demand erosion. Los Angeles, where I’m based, has been losing domestic residents for years. What held the market together was a steady stream of international arrivals — economic immigrants, asylum seekers, TPS holders — who absorbed workforce housing units, filled multifamily vacancies, and supported retail and service demand. That engine is sputtering. If you’re a multifamily owner in a heavily immigrant-dependent submarket in LA or Miami, your effective demand pool just got smaller, and it’s not coming back quickly.

The Sun Belt divergence is real and accelerating. Austin, Raleigh, Boise, Myrtle Beach, Wilmington — these markets are growing at four times the national rate or better. The domestic migration trends feeding these markets predate Trump’s second term. What’s changed is that the immigration slowdown is now amplifying the relative advantage of Sun Belt metros that weren’t as dependent on international arrivals in the first place. Raleigh and the Research Triangle were already on a structural growth trajectory driven by tech and life sciences relocation. They don’t need a wave of asylum seekers to fill units — they’ve got corporate relocations and strong domestic in-migration doing the work.

Workforce and affordable housing demand is bifurcating. The policy environment is creating two different stories simultaneously. In immigrant-dependent markets, the demand destruction at the lower end of the rent stack is real — owners of naturally occurring affordable housing (NOAH) assets in LA and Miami should be paying attention to rising vacancy in that segment. But in growth markets, workforce housing demand is, if anything, intensifying, because domestic in-migrants arrive with jobs and income but still get priced out of new Class A product.

This is exactly why our Oldivai platform is focused on workforce housing in secondary and tertiary markets. The capital-per-door equation works. The demand fundamentals hold. And the political risk profile is dramatically lower.

Border metros are getting hit hardest. Laredo and Yuma saw some of the sharpest percentage drops in population growth rates of any market in the country. These are thin markets to begin with — the economic base is trade, logistics, and border-dependent commerce. If you have exposure there, you need a realistic thesis for what fills that demand gap, because policy-driven demographic reversal in border communities is not a short-term phenomenon.

The Macro Frame

There’s a debate in real estate circles right now about whether the coastal markets are in a temporary trough or something more durable. I’m firmly in the structural camp — and not because I’m bearish on cities.

The conditions that enabled coastal markets to absorb chronic domestic outmigration were unusual: a historically anomalous period of high immigration, loose monetary policy that kept institutional capital flowing into gateway market cap rates, and a long cultural narrative that “you have to be in New York or LA to matter.” All three of those conditions are weakening at the same time.

Meanwhile, the mid-size metros winning right now — Raleigh, Boise, Bozeman, Asheville, the Carolinas broadly — are winning on fundamentals: lower cost of living, strong job creation, and increasingly, amenity-rich quality of life that competes with the coasts. Remote work didn’t create this trend, but it permanently accelerated it.

For us as developers and investors, the playbook writes itself: follow the demographic momentum, build where the demand is going rather than where it used to be, and price risk accordingly in markets that are structurally dependent on policy regimes you can’t control.

The Census Bureau gave you the map. Now you have to decide where to build.

Daniel Kaufman is a principal and CEO of Kaufman & Company, a real estate development and investment firm with 25+ years of experience across multifamily, workforce housing, mixed-use, and resort development. The Kaufman Report covers real estate, capital markets, and the forces shaping where and how America builds.