The headlines will tell you the rental market is normalizing. Rents are down. Vacancies are up. Supply is coming online. Breathe easy.

Don’t.

Harvard’s Joint Center for Housing Studies just dropped its America’s Rental Housing 2026 report, and if you read past the headline numbers, what you find isn’t a market healing — it’s a market splitting in two. And the bottom half is losing badly.

The Numbers First

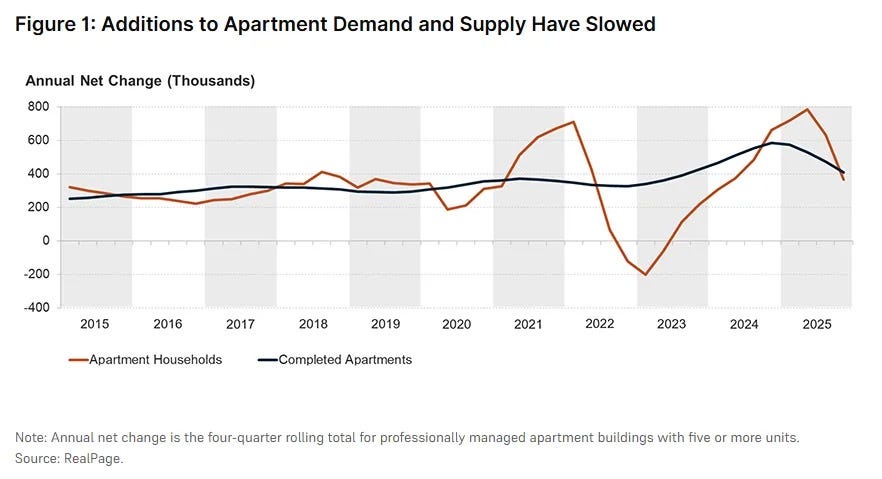

Rental demand surged in early 2025, then fell off a cliff by Q4. New apartment households dropped from 784,000 mid-year to 366,000 by year-end. That’s not a soft landing — that’s a labor market spooked economy pulling back in real time.

Asking rents on professionally managed apartments fell 0.6% year-over-year by Q4 2025. The South and West took the biggest hits. Meanwhile, multifamily starts came in at 416,000 for the year, and the units-under-construction pipeline dropped from 996,000 in 2023 to 686,000 in 2025. The construction wave is receding.

On paper, that looks like equilibrium finding itself.

It isn’t.

The K-Shape Nobody Wants to Talk About

Analyst Jay Parsons has been calling this correctly: today’s rental market isn’t one market. It’s two, stacked on top of each other and pretending to be one.

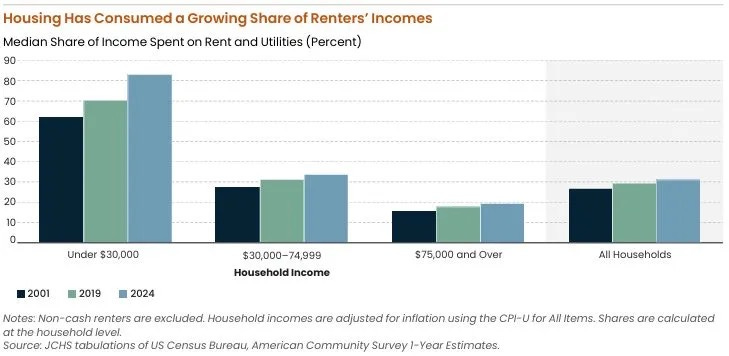

Top half: Higher-income renters — households earning $75K+ — are driving nearly all new renter household formation. They’re living in Class A and B product and spending roughly 20% of their income on rent. They’re fine.

Bottom half: Lower-income renters are routinely spending over half their income on housing. They’re competing for a shrinking pool of Class C and subsidized units, and losing.

22.7 million renter households are cost-burdened — that’s a record. Nearly 50% of all renters are spending more than 30% of income on housing. Over 12 million are severely cost-burdened, north of 50%. These aren’t abstractions. These are people who can’t absorb a medical bill, a car repair, or a rent increase without something else breaking.

The Affordable Stock Is Vanishing and Nobody Is Replacing It

This is the structural story that the “rents are cooling” narrative completely obscures.

From 2014 to 2024, the U.S. lost 9.3 million units renting below $1,400/month — including 2.5 million units under $600. In the same period, the number of units renting at $1,400 or more grew by 11.8 million.

The market isn’t just failing to produce affordable housing. It’s actively consuming what little remains. Naturally occurring affordable housing — the aging Class C stock that has always served working-class renters — is being renovated, converted, or demolished upmarket faster than any policy intervention can offset it.

And the new supply coming online? It’s almost entirely targeting the top of the market. Because that’s where the math pencils. That’s not a criticism of developers — I’m one of them. It’s an indictment of a financing and regulatory environment that has made workforce and affordable product functionally impossible to build at scale without subsidy.

Policy Is Moving. Not Fast Enough.

Credit where it’s due: there are signals of policy momentum. Federal Low-Income Housing Tax Credit allocations expanded. HUD’s budget got a boost. The ROAD to Housing Act is moving to expand supply and modernize program delivery. State and local governments are experimenting with new financing tools, zoning reform, and mixed-income development frameworks.

But let’s be honest about the velocity here. The policy response is incremental. The problem is structural and accelerating. And recent cuts to SNAP and Medicaid are hitting the same households already spending 50%+ of income on rent — compressing budgets that had no room left to compress.

What This Means If You’re Operating in This Market

If you’re a developer, the headline risk isn’t rent softness — it’s the Class A/B markets where new supply has outpaced demand absorption. Lease-up timelines are stretching. Concessions are back. Underwrite conservatively.

If you’re playing in workforce and affordable, the fundamentals are actually stronger than the headlines suggest — constrained supply, persistent demand, and a growing policy tailwind. The challenge remains execution: construction costs, entitlements, and capital stack complexity haven’t gotten easier.

If you’re a policymaker or an advocate citing the “cooling market” as evidence that things are improving — you’re looking at the wrong half of the split screen.

The Bottom Line

The rental market is cooling at the top. It is not cooling for the 22.7 million households who are cost-burdened, or the 12 million who are severely cost-burdened, or the working-class renters watching their $800/month apartment get renovated into something they can no longer afford.

A K-shaped market that “stabilizes” means the top stabilizes. The bottom keeps falling.

That’s not normalization. That’s bifurcation becoming permanent.

— Daniel Kaufman

The Kaufman Report